Berkshire Hathaway 2007 Annual Report Download - page 4

Download and view the complete annual report

Please find page 4 of the 2007 Berkshire Hathaway annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

|

|

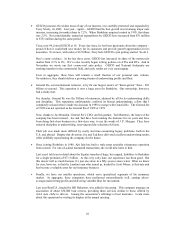

BERKSHIRE HATHAWAY INC.

To the Shareholders of Berkshire Hathaway Inc.:

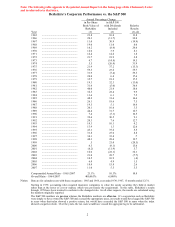

Our gain in net worth during 2007 was $12.3 billion, which increased the per-share book value of

both our Class A and Class B stock by 11%. Over the last 43 years (that is, since present management took

over) book value has grown from $19 to $78,008, a rate of 21.1% compounded annually.*

Overall, our 76 operating businesses did well last year. The few that had problems were primarily

those linked to housing, among them our brick, carpet and real estate brokerage operations. Their setbacks

are minor and temporary. Our competitive position in these businesses remains strong, and we have first-

class CEOs who run them right, in good times or bad.

Some major financial institutions have, however, experienced staggering problems because they

engaged in the “weakened lending practices” I described in last year’ s letter. John Stumpf, CEO of Wells

Fargo, aptly dissected the recent behavior of many lenders: “It is interesting that the industry has invented

new ways to lose money when the old ways seemed to work just fine.”

You may recall a 2003 Silicon Valley bumper sticker that implored, “Please, God, Just One More

Bubble.” Unfortunately, this wish was promptly granted, as just about all Americans came to believe that

house prices would forever rise. That conviction made a borrower’ s income and cash equity seem

unimportant to lenders, who shoveled out money, confident that HPA – house price appreciation – would

cure all problems. Today, our country is experiencing widespread pain because of that erroneous belief.

As house prices fall, a huge amount of financial folly is being exposed. You only learn who has been

swimming naked when the tide goes out – and what we are witnessing at some of our largest financial

institutions is an ugly sight.

Turning to happier thoughts, we can report that Berkshire’ s newest acquisitions of size, TTI and

Iscar, led by their CEOs, Paul Andrews and Jacob Harpaz respectively, performed magnificently in 2007.

Iscar is as impressive a manufacturing operation as I’ ve seen, a view I reported last year and that was

confirmed by a visit I made in the fall to its extraordinary plant in Korea.

Finally, our insurance business – the cornerstone of Berkshire – had an excellent year. Part of the

reason is that we have the best collection of insurance managers in the business – more about them later.

But we also were very lucky in 2007, the second year in a row free of major insured catastrophes.

That party is over. It’ s a certainty that insurance-industry profit margins, including ours, will fall

significantly in 2008. Prices are down, and exposures inexorably rise. Even if the U.S. has its third

consecutive catastrophe-light year, industry profit margins will probably shrink by four percentage points

or so. If the winds roar or the earth trembles, results could be far worse. So be prepared for lower

insurance earnings during the next few years.

Yardsticks

Berkshire has two major areas of value. The first is our investments: stocks, bonds and cash

equivalents. At yearend these totaled $141 billion (not counting those in our finance or utility operations,

which we assign to our second bucket of value).

*All per-share figures used in this report apply to Berkshire’ s A shares. Figures for the B shares

are 1/30th of those shown for the A.

3