Berkshire Hathaway 2008 Annual Report Download - page 17

Download and view the complete annual report

Please find page 17 of the 2008 Berkshire Hathaway annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

|

|

Investors should be skeptical of history-based models. Constructed by a nerdy-sounding priesthood

using esoteric terms such as beta, gamma, sigma and the like, these models tend to look impressive. Too often,

though, investors forget to examine the assumptions behind the symbols. Our advice: Beware of geeks bearing

formulas.

************

A final post-script on BHAC: Who, you may wonder, runs this operation? While I help set policy, all

of the heavy lifting is done by Ajit and his crew. Sure, they were already generating $24 billion of float along

with hundreds of millions of underwriting profit annually. But how busy can that keep a 31-person group?

Charlie and I decided it was high time for them to start doing a full day’s work.

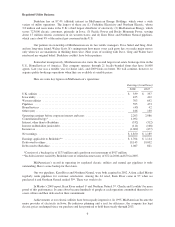

Investments

Because of accounting rules, we divide our large holdings of common stocks this year into two

categories. The table below, presenting the first category, itemizes investments that are carried on our balance

sheet at market value and that had a yearend value of more than $500 million.

12/31/08

Shares Company

Percentage of

Company

Owned Cost* Market

(in millions)

151,610,700 American Express Company .................... 13.1 $ 1,287 $ 2,812

200,000,000 The Coca-Cola Company ....................... 8.6 1,299 9,054

84,896,273 ConocoPhillips ............................... 5.7 7,008 4,398

30,009,591 Johnson & Johnson ........................... 1.1 1,847 1,795

130,272,500 Kraft Foods Inc. .............................. 8.9 4,330 3,498

3,947,554 POSCO ..................................... 5.2 768 1,191

91,941,010 The Procter & Gamble Company ................. 3.1 643 5,684

22,111,966 Sanofi-Aventis ............................... 1.7 1,827 1,404

11,262,000 Swiss Re .................................... 3.2 773 530

227,307,000 Tesco plc ................................... 2.9 1,326 1,193

75,145,426 U.S. Bancorp ................................ 4.3 2,337 1,879

19,944,300 Wal-Mart Stores, Inc. .......................... 0.5 942 1,118

1,727,765 The Washington Post Company .................. 18.4 11 674

304,392,068 Wells Fargo & Company ....................... 7.2 6,702 8,973

Others ...................................... 6,035 4,870

Total Common Stocks Carried at Market .......... $37,135 $49,073

*This is our actual purchase price and also our tax basis; GAAP “cost” differs in a few cases because of

write-ups or write-downs that have been required.

In addition, we have holdings in Moody’s and Burlington Northern Santa Fe that we now carry at

“equity value” – our cost plus retained earnings since our purchase, minus the tax that would be paid if those

earnings were paid to us as dividends. This accounting treatment is usually required when ownership of an

investee company reaches 20%.

We purchased 15% of Moody’s some years ago and have not since bought a share. Moody’s, though,

has repurchased its own shares and, by late 2008, those repurchases reduced its outstanding shares to the point

that our holdings rose above 20%. Burlington Northern has also repurchased shares, but our increase to 20%

primarily occurred because we continued to buy this stock.

15