Berkshire Hathaway 2013 Annual Report Download - page 5

Download and view the complete annual report

Please find page 5 of the 2013 Berkshire Hathaway annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

|

|

BERKSHIRE HATHAWAY INC.

To the Shareholders of Berkshire Hathaway Inc.:

Berkshire’s gain in net worth during 2013 was $34.2 billion. That gain was after our deducting $1.8 billion

of charges – meaningless economically, as I will explain later – that arose from our purchase of the minority

interests in Marmon and Iscar. After those charges, the per-share book value of both our Class A and Class B stock

increased by 18.2%. Over the last 49 years (that is, since present management took over), book value has grown

from $19 to $134,973, a rate of 19.7% compounded annually.*

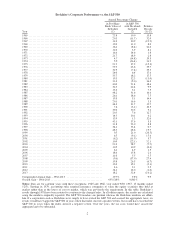

On the facing page, we show our long-standing performance measurement: The yearly change in

Berkshire’s per-share book value versus the market performance of the S&P 500. What counts, of course, is per-

share intrinsic value. But that’s a subjective figure, and book value is useful as a rough tracking indicator. (An

extended discussion of intrinsic value is included in our Owner-Related Business Principles on pages 103 - 108.

Those principles have been included in our reports for 30 years, and we urge new and prospective shareholders to

read them.)

As I’ve long told you, Berkshire’s intrinsic value far exceeds its book value. Moreover, the difference has

widened considerably in recent years. That’s why our 2012 decision to authorize the repurchase of shares at 120%

of book value made sense. Purchases at that level benefit continuing shareholders because per-share intrinsic value

exceeds that percentage of book value by a meaningful amount. We did not purchase shares during 2013, however,

because the stock price did not descend to the 120% level. If it does, we will be aggressive.

Charlie Munger, Berkshire’s vice chairman and my partner, and I believe both Berkshire’s book value and

intrinsic value will outperform the S&P in years when the market is down or moderately up. We expect to fall

short, though, in years when the market is strong – as we did in 2013. We have underperformed in ten of our 49

years, with all but one of our shortfalls occurring when the S&P gain exceeded 15%.

Over the stock market cycle between yearends 2007 and 2013, we overperformed the S&P. Through full

cycles in future years, we expect to do that again. If we fail to do so, we will not have earned our pay. After all, you

could always own an index fund and be assured of S&P results.

The Year at Berkshire

On the operating front, just about everything turned out well for us last year – in certain cases very well.

Let me count the ways:

ŠWe completed two large acquisitions, spending almost $18 billion to purchase all of NV Energy and a

major interest in H. J. Heinz. Both companies fit us well and will be prospering a century from now.

With the Heinz purchase, moreover, we created a partnership template that may be used by Berkshire in

future acquisitions of size. Here, we teamed up with investors at 3G Capital, a firm led by my friend, Jorge

Paulo Lemann. His talented associates – Bernardo Hees, Heinz’s new CEO, and Alex Behring, its

Chairman – are responsible for operations.

* All per-share figures used in this report apply to Berkshire’s A shares. Figures for the B shares are

1/1500th of those shown for A.

3