Caremark 2003 Annual Report Download - page 45

Download and view the complete annual report

Please find page 45 of the 2003 Caremark annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52

|

|

4. Two satellite office facilities (the “Satellite Facilities”)

would be closed and their operations would be

consolidated into the Company’s Woonsocket,

Rhode Island corporate headquarters by no later

than December 2001. Since these locations were

leased facilities, management planned to either return

the premises to the landlords at the conclusion of

the leases or negotiate an early termination of the

contractual obligations. The Satellite Facilities were

closed in December 2001.

5. Approximately 1,500 managerial, administrative and

store employees in the Company’s Woonsocket, Rhode

Island corporate headquarters; Columbus Mail Facility;

Henderson D.C. and the Stores would be terminated.

As of April 30, 2002, all of these employees had

been terminated.

In accordance with Emerging Issues Task Force (“EITF”)

Issue 94-3, “Liability Recognition for Certain Employee

Termination Benefits and Other Costs to Exit an Activity

(Including Certain Costs Incurred in a Restructuring),”

SFAS No. 121 and Staff Accounting Bulletin No. 100,

“Restructuring and Impairment Charges,” the Company

recorded a $346.8 million pre-tax charge ($226.9 million

after-tax) to operating expenses during the fourth quarter

of 2001 for restructuring and asset impairment costs.

In accordance with Accounting Research Bulletin No. 43,

“Restatement and Revision of Accounting Research

Bulletins,” the Company also recorded a $5.7 million

pre-tax charge ($3.6 million after-tax) to cost of goods

sold during the fourth quarter of 2001 to reflect the

markdown of certain inventory contained in the Stores

to its net realizable value. In total, the restructuring

and asset impairment charge was $352.5 million pre-tax

($230.5 million after-tax), or $0.56 per diluted share in

2001 (the “Restructuring Charge”). The aggregate impact

of the 229 stores on the Company’s consolidated financial

statements for the year ended December 29, 2001, totaled

$585.3 million in net sales and $13.7 million in operating

losses, which included depreciation and amortization

of $12.4 million, incremental markdowns incurred in

connection with liquidating inventory and incremental

payroll and other store-related costs incurred in connection

with closing and/or preparing the 229 stores for closing.

Whenever possible, the Company attempts to transfer the

customer base of its closed stores to adjacent CVS store

locations. The Company’s success in retaining customers

and the related impact on the above revenue and operating

income or loss, however, cannot be precisely calculated.

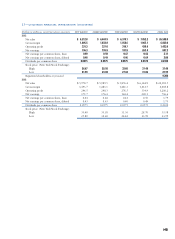

Following is a summary of the significant components of

the Restructuring Charge:

In millions

Noncancelable lease obligations $ 227.4

Asset write-offs 105.6

Employee severance and benefits 19.5

To t a l (1) $ 352.5

(1) The Restructuring Charge is comprised of $5.7 million

recorded in cost of goods sold and $346.8 million recorded

in selling, general and administrative expenses.

The Restructuring Charge will require total cash payments

of $246.9 million. The remaining Restructuring Charge

liability totaled $168.9 million as of January 3, 2004 and

$192.1 million as of December 28, 2002. The remaining

liability in both years primarily consisted of future cash

payments for noncancelable lease obligations extending

through 2024. The Company believes that the reserve

balances as of January 3, 2004 are adequate to cover the

remaining liabilities associated with the Restructuring Charge.

Noncancelable lease obligations included $227.4 million

for the estimated continuing lease obligations of the Stores,

the Mail Facility and the Satellite Facilities. As required

by EITF Issue 88-10, “Costs Associated with Lease

Modification or Termination,” the estimated continuing

lease obligations were reduced by estimated probable

sublease rental income.

Asset write-offs included $59.0 million for fixed asset

write-offs, $40.9 million for intangible asset write-offs

and $5.7 million for the markdown of certain inventory

to its net realizable value. The fixed asset and intangible

asset write-offs relate to the Stores, the Mail Facility

and the Satellite Facilities. Management’s decision to

close the above locations was considered to be an event

or change in circumstances as defined in SFAS No. 121.

Since management intended to use the Stores and the Mail

Facility on a short-term basis during the shutdown period,

impairment was measured using the “Assets to Be Held

and Used” provisions of SFAS No. 121. The analysis

was prepared at the individual location level, which is

the lowest level at which individual cash flows can be

identified. The analysis first compared the carrying amount

of the location’s assets to the location’s estimated future

cash flows (undiscounted and without interest charges)

through the anticipated closing date. If the estimated future

cash flows used in this analysis were less than the carrying

amount of the location’s assets, an impairment loss

calculation was prepared. The impairment loss calculation

compared the carrying value of the location’s assets to the

location’s estimated future cash flows (discounted and with

(43)