DTE Energy 2008 Annual Report Download - page 18

Download and view the complete annual report

Please find page 18 of the 2008 DTE Energy annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

-

30

-

31

-

32

-

33

|

|

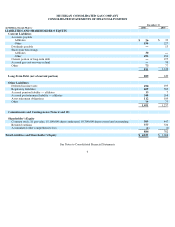

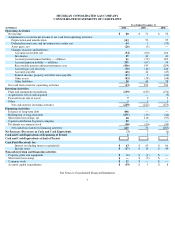

LIABILITIES

Uncollectible Expense True-Up Mechanism (UETM) and Report of Safety and Training-Related Expenditures

2005 UETM — In March 2006, MichCon filed an application with the MPSC for approval of its UETM for 2005. MichCon’s 2005 base rates

included $37 million for anticipated uncollectible expenses. Actual 2005 uncollectible expenses totaled $60 million. The true-up mechanism

allowed MichCon to recover 90% of uncollectibles that exceeded the $37 million base. Under the formula prescribed by the MPSC, MichCon

recorded an under-recovery of approximately $11 million for uncollectible expenses from May 2005 (when the mechanism took effect) through

the end of 2005. In December 2006, the MPSC issued an order authorizing MichCon to implement the UETM monthly surcharge for service

rendered on and after January 1, 2007.

As part of the March 2006 application with the MPSC, MichCon filed a review of its 2005 annual safety and training-related expenditures.

MichCon reported that actual safety and training-related expenditures for the initial period exceeded the pro-rata amounts included in base rates

and, based on the under-recovered position, recommended no refund at that time. In the December 2006 order, the MPSC also approved

MichCon’s 2005 safety and training report. On October 14, 2008, the State of Michigan Court of Appeals rejected the appeal of the Attorney

General of the State of Michigan upholding the right of the MPSC to authorize MichCon to charge the 2005 UETM.

2006 UETM — In March 2007, MichCon filed an application with the MPSC for approval of its UETM for 2006 requesting $33 million of

under-recovery plus applicable carrying costs of $3 million. The March 2007 application included a report of MichCon’s 2006 annual safety

and training-related expenditures, which showed a $2 million over-recovery. In August 2007, MichCon filed revised exhibits reflecting an

agreement with the MPSC Staff to net the $2 million over-recovery and associated interest related to the 2006 safety and training-related

expenditures against the 2006 UETM under-recovery. An MPSC order was issued in December 2007 approving the collection of $33 million

requested in the August 2007 revised filing. MichCon was authorized to implement the new UETM monthly surcharge for service rendered on

and after January 1, 2008.

2007 UETM — In March 2008, MichCon filed an application with the MPSC for approval of its UETM for 2007 requesting approximately

$34 million consisting of $33 million of costs related to 2007 uncollectible expense and associated carrying charges and $1 million of under-

collections for the 2005 UETM. The March 2008 application included a report of MichCon’s 2007 annual safety and training-related expenses,

which showed no refund was necessary because actual expenditures exceeded the amount included in base rates. An MPSC order was issued in

December 2008 approving the collection of $34 million requested in the March 2008 filing. MichCon was authorized to implement the new

UETM monthly surcharge for service rendered on and after January 1, 2009.

Gas Cost Recovery Proceedings

2005-2006 Plan Year — In June 2006, MichCon filed its GCR reconciliation for the 2005-2006 GCR year. The filing supported a total over-

recovery, including interest through March 2006, of $13 million. MPSC Staff and other intervenors filed testimony regarding the reconciliation

in which they recommended disallowances related to MichCon’s implementation of its dollar cost averaging fixed price program. In

January 2007, MichCon filed testimony rebutting these recommendations. In December 2007, the MPSC issued an order

16

•

A

sset removal costs — The amount collected from customers for the funding of future asset removal activities.

•

R

efundable income taxes — Income taxes refundable to our customers representing the difference in property-related deferred income taxes

payable and amounts recognized pursuant to MPSC authorization.

•

A

ccrued GCR refund — Liability for the temporary over-recovery of and a return on gas costs incurred by MichCon which are recoverable

through the GCR mechanism.

•

N

egative pension offset — The Company’s negative pension costs are not included as a reduction to its authorized rates; therefore, the

Company is accruing a regulatory liability to eliminate the impact on earnings of the negative pension expense accrued. This regulatory

liability will reverse to the extent the Company’s pension expense is positive in future years.

•

D

eferred income taxes — Michigan Business Tax — In July 2007, the MBT was enacted by the State of Michigan. State deferred tax assets

were established, and offsetting regulatory liabilities were recorded as the impacts of the deferred tax assets will be reflected in rates.