HP 2007 Annual Report Download - page 58

Download and view the complete annual report

Please find page 58 of the 2007 HP annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

|

|

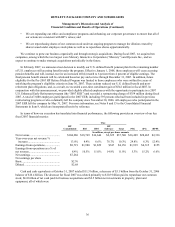

HEWLETT-PACKARD COMPANY AND SUBSIDIARIES

Management’s Discussion and Analysis of

Financial Condition and Results of Operations (Continued)

estimate the impact, if any, that SFAS 159 will have on our consolidated results of operations and financial condition.

In June 2007, the FASB also ratified EITF 07-3, “Accounting for Nonrefundable Advance Payments for Goods or

Services Received for Use in Future Research and Development Activities” (“EITF 07-3”). EITF 07-3 requires that

nonrefundable advance payments for goods or services that will be used or rendered for future research and development

activities be deferred and capitalized and recognized as an expense as the goods are delivered or the related services are

performed. EITF 07-3 is effective, on a prospective basis, for fiscal years beginning after December 15, 2007 and will be

adopted by us in the first quarter of fiscal 2009. We do not expect the adoption of EITF 07-3 to have a material effect on our

consolidated results of operations and financial condition.

In December 2007, the FASB issued SFAS No. 141 (revised 2007), “Business Combinations” (“SFAS 141R”).

SFAS 141R establishes principles and requirements for how an acquirer recognizes and measures in its financial statements

the identifiable assets acquired, the liabilities assumed, any noncontrolling interest in the acquiree and the goodwill acquired.

SFAS 141R also establishes disclosure requirements to enable the evaluation of the nature and financial effects of the

business combination. SFAS 141R is effective as of the beginning of an entity’ s fiscal year that begins after December 15,

2008, and will be adopted by us in the first quarter of fiscal 2010. We are currently evaluating the potential impact, if any, of

the adoption of SFAS 141R on our consolidated results of operations and financial condition.

In December 2007, the FASB issued SFAS No. 160, “Noncontrolling Interests in Consolidated Financial Statements—an

amendment of Accounting Research Bulletin No. 51” (“SFAS 160”). SFAS 160 establishes accounting and reporting

standards for ownership interests in subsidiaries held by parties other than the parent, the amount of consolidated net income

attributable to the parent and to the noncontrolling interest, changes in a parent’ s ownership interest and the valuation of

retained noncontrolling equity investments when a subsidiary is deconsolidated. SFAS 160 also establishes disclosure

requirements that clearly identify and distinguish between the interests of the parent and the interests of the noncontrolling

owners. SFAS 160 is effective as of the beginning of an entity’ s fiscal year that begins after December 15, 2008, and will be

adopted by us in the first quarter of fiscal 2010. We are currently evaluating the potential impact, if any, of the adoption of

SFAS 160 on our consolidated results of operations and financial condition.

In addition to the SFAS 158 adoption mentioned above, we adopted the following accounting standards in fiscal 2007,

none of which had a material effect on our consolidated results of operations during such period or financial condition at the

end of such period:

• SFAS No. 154, “Accounting for Changes and Error Corrections”;

• Staff Accounting Bulletin No. 108, “Considering the Effects of Prior Year Misstatements when Quantifying

Misstatements in Current Year Financial Statements”;

• EITF 05-5, “Accounting for Early Retirement or Postemployment Programs with Specific Features (Such as Terms

Specified in Altersteilzeit Early Retirement Arrangements)”; and

• EITF 06-9, “Reporting a Change in (or the Elimination of) a Previously Existing Difference between the Fiscal Year

End of a Parent Company and That of a Consolidated Entity or between the Reporting Period of an Investor and

That of an Equity Method Investee.”

44