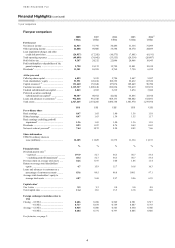

HSBC 2008 Annual Report Download - page 16

Download and view the complete annual report

Please find page 16 of the 2008 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

|

|

HSBC HOLDINGS PLC

Report of the Directors: Operating and Financial Review (continued)

Challenges and uncertainties

14

presenting challenges to HSBC which are specific

to those areas.

Europe

In the UK, the economy has entered recession and

the currency has fallen in value against the US

dollar, the yen and the euro. Changes in the

marketplace are emerging following the part-

nationalisation of some major financial institutions,

and political interaction with the regulatory

environment is becoming more frequent as the

government seeks to stimulate lending to preserve

economic activity. A period of low interest rates will

reduce deposit spreads and HSBC’s retail business

model will be more dependent on transactional fees

and lending margin. Pension funding requirements,

in particular for UK defined benefit schemes, will

place increased financing demands on corporates,

which may lead to unfunded commitments being

drawn down, adding to pressure on system liquidity.

The recent deterioration in credit quality is expected

to continue as the economy contracts, with loan

impairment charges rising as a result. Market

volatility is also expected to continue.

In France, changes in the marketplace are slowly

emerging following government measures to

stimulate lending and preserve economic activity. A

period of low interest rates will not adversely impact

spreads in the short-term but will have an adverse

effect in later years. HSBC’s retail business model is

dependent on banking fees to maintain profitability

and a recovery in financial markets is necessary in

order to enhance brokerage and management fees

and stimulate fund management activities.

Deterioration in credit quality is expected to

continue as the economy contracts, with commercial

loan impairment charges rising as a result. Personal

loan impairment charges are expected to remain at

around current levels unless there is a very deep

recession.

Conditions are likely to remain difficult in a

number of markets in which HSBC currently trades

and volatility is expected to continue.

Hong Kong and Rest of Asia-Pacific

In Asia-Pacific, a prolonged period of low interest

rates is expected which will put pressure on HSBC’s

net interest income from its strong deposit base.

With capital market and currency volatility endemic,

customers are likely to seek capital protection and

become increasingly rate and risk sensitive, seeking

out products which offer deposit insurance and

government guarantees. Regulatory reforms in the

areas of wealth management product complexity,

sales requirements and liquidity and reserve ratios

are likely, and these will lead to a higher cost of

compliance, greater standardisation and slower

product approvals. International trade is expected to

continue to contract, affecting import and export

volumes and reducing HSBC’s earnings from trade

financing. The quality of the asset book will

deteriorate if economic factors beyond HSBC’s

control do not improve, reducing customer credit

ratings and, as a consequence, increasing risk-

weighted asset allocations and capital requirements.

This could be exacerbated if capital continues to be

repatriated from emerging markets to more

developed economies to take advantage of lower

asset prices, adversely affecting emerging markets’

balance of payments and foreign exchange reserves.

However, Asia is expected to adapt quickly to secure

recovery from the global recession, led by mainland

China and India.

The fall in global demand for oil products and

related prices, and the contraction in financial

surpluses held by key oil-producing countries

following the declines in capital markets, will reduce

the ability of some countries in the Middle East to

maintain spending, borrowing and investment

domestically and internationally. This will result in

the cancellation or postponement of infrastructure

projects which, together with weakening property

prices, is expected to reduce both credit cover and

revenue streams for financial institutions. The

availability of economically priced, long-term

funding is likely to contract. Business activity and

private investment will also slow as consumer

confidence declines. These factors will combine to

place pressure on net revenues and on capital

requirements.

North America

In the US, the steep decline in the housing market,

with falling home prices and increasing foreclosures,

and rising unemployment have resulted in significant

write-downs of loans and advances and mortgage-

backed securities. The effect of these write-downs

subsequently spread to other capital market

activities, leading many financial institutions to seek

additional capital, merge with larger and stronger

institutions and, in some cases, fail. Many lenders

reduced or stopped providing funding to borrowers,

including to other financial institutions. This market

turmoil and resultant tightening of credit have led to

an increased level of delinquencies, a fall in

consumer confidence, increased market volatility

and a widespread reduction in business activity in

general. To date, various government intervention

measures designed to stabilise the markets, including