HSBC 2014 Annual Report Download - page 13

Download and view the complete annual report

Please find page 13 of the 2014 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

|

|

HSBC BANK PLC

Strategic Report: Strategic Priorities (continued)

11

• capturing growth opportunities in home and priority

growth markets, particularly from group collaboration

by accessing owners and principals of CMB and

GB&M clients; and

• repositioning the business to concentrate on onshore

markets and a smaller number of target offshore

markets, aligned with Group priorities.

Implementing Global Standards, enhancing risk

management controls, tax transparency and simplifying

processes also remain top priorities for GPB.

Key Performance Indicators

The Board of Directors tracks the group’s progress in

implementing its strategy with a range of financial and

non-financial measures or key performance indicators.

Progress is assessed by comparison with the group

strategic priorities, operating plan targets and historical

performance.

From time to time the group reviews its key performance

indicators (‘KPIs’) in light of its strategic objectives and

may adopt new or refined measures to better align the

KPIs to HSBC’s strategy and strategic priorities.

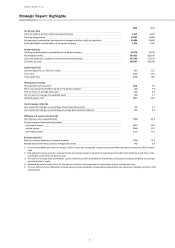

Financial KPIs

2014

2013

%

%

Risk adjusted revenue growth

(3.6)

5.6

Cost efficiency ratio

79.8

66.8

Pre

-tax return on average risk-

weighted

assets

ratio

0.8

1.7

CET 1 / Core tier 1 capital ratio

8.7

12.1

Risk-adjusted revenue growth is measured as the

percentage change in reported net operating income

after loan impairment and other credit risk charges since

last year. The group seeks to deliver consistent growth in

risk-adjusted revenues.

Outcome: Reported risk-adjusted revenue growth

decreased primarily due to weaker trading income

compared to 2013.

Cost efficiency ratio is measured as total operating

expenses divided by net operating income before loan

impairment and other credit risk provisions.

Outcome: The cost efficiency ratio increased principally

due to higher costs, most notably from charges for

investigations into foreign exchange, combined with

lower overall revenues.

Pre-tax return on average risk-weighted assets ratio is

measured as pre-tax profit divided by average risk-

weighted assets. The group targets a return in the

medium term of between 1.8 and 2.0 per cent.

Outcome: The return on average risk-weighted assets

was significantly below the target range predominantly

due to a fall in profit before tax.

Common equity tier / Core tier 1 capital ratio –

represents the ratio of common equity tier / core tier 1

capital comprising shareholders’ equity and related non-

controlling interests less regulatory deductions and

adjustments to total risk weighted assets. The group

seeks to maintain a strong capital base to support the

development of its business and meet regulatory capital

requirements at all times.

Outcome: The Common Equity Tier 1 ratio fell compared

to Core Tier 1 ratio from 12.1 to 8.7 per cent primarily

reflecting the impact of the transition to CRD IV.

Employee engagement

Strong employee engagement leads to positive

commercial outcomes and underpins improved business

performance, increased customer satisfaction, higher

productivity, talent retention and reduced absenteeism.

We assess our employees’ engagement through our

Global People Surveys, which were held annually from

2007 to 2011 and bi-annually thereafter. The latest

Survey, in 2013, focused on supporting a values-led high

performance culture by assessing if our employees were

engaged in the Group’s purpose and felt able to deliver

on our ambition to become the world’s leading

international bank.

The overall Europe engagement score in 2013 was 60 per

cent, which was below the financial services norm.

Strong scores were registered in risk awareness (78 per

cent, 5 percentage points above the external best-in-

class), employee development (58 per cent), leadership

capability (58 per cent) and living the HSBC Values (78

per cent). Aspects that require concerted attention

included pride and advocacy, which had fallen from 2011

levels. The next Global People Survey will be conducted

in 2015.

Brand value

HSBC monitors the strength of its brand through an

empirical tool (the Brand Equity Index), which combines

measurements of perception for customer purchase

consideration from the brand, customer advocacy of the

brand and emotional connection to the brand to develop

an Index Value that can be tracked over time.

The HSBC brand in the UK scores at the competitive

average, ranking third, and is strongly differentiated

from an International perspective. In both Turkey and

France, HSBC's Brand Equity Index improved during 2014

but is below the average of its larger local competitors.

Customer service and satisfaction

In RBWM, customer satisfaction is measured through an

independent market research survey of retail banking

customers, using a Customer Recommendation Index

(‘CRI’) to score performance. In the UK during 2014 our

CRI ranking was poor and for the first half of the year,

the bank achieved historic low scores. Following a strong

intervention programme in our service channel

'Simplifying Growth' we saw a positive response and

finished the year with a very good fourth quarter

position ranking us joint third behind Halifax and

Santander. Turkey and France both saw significant

improvement throughout the year and both achieved

their targets to improve their overall score relative to the

competitor average. Turkey in particular finished the

fourth quarter strongly with a record competitive joint

third position in the market.

Throughout 2014, CMB continued to draw insight and

metrics from the Client Engagement Programme (‘CEP’),

conducted by an independent third party. The results