PG&E 2015 Annual Report Download - page 89

Download and view the complete annual report

Please find page 89 of the 2015 PG&E annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

|

|

81

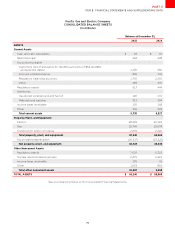

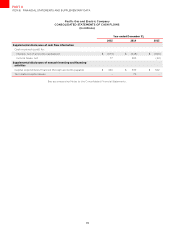

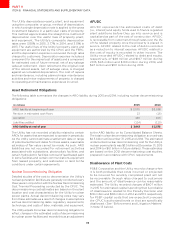

PART II

ITEM 8.FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA

Computing Arrangement, which adds guidance to help

entities evaluate the accounting treatment for cloud

computing arrangements. The ASU became eective for

PG&E Corporation and the Utility on January 1, 2016. PG&E

Corporation and the Utility have determined that this ASU

will not impact their consolidated financial statements and

related disclosures and will adopt this standard starting in

the first quarter of 2016.

Presentation of Debt Issuance Costs

In April 2015, the FASB issued ASU No. 2015-03, Interest -

Imputation of Interest (Subtopic 835-30): Simplifying the

Presentation of Debt Issuance Costs, which amends existing

presentation of debt issuance costs. PG&E Corporation

and the Utility currently disclose debt issuance costs in

current assets – other and noncurrent assets – other. The

amendments in this ASU, that became eective for PG&E

Corporation and the Utility on January 1, 2016, require that

debt issuance costs related to a recognized debt liability

be presented in the balance sheet as a direct deduction

from the carrying amount of that debt liability, consistent

with debt discounts. PG&E Corporation and the Utility will

adopt this standard in the first quarter of 2016 and do

not expect the reclassification to have a material impact

on their consolidated financial statements.

Revenue Recognition Standard

In May 2014, the FASB issued ASU No. 2014-09, Revenue from

Contracts with Customers, which amends existing revenue

recognition guidance. In August 2015, the FASB issued ASU

No. 2015-14, Revenue from Contracts with Customers (Topic

606): Deferral of the Eective Date, deferring the eective

date of this amendment for PG&E Corporation and the

Utility by one year to January 1, 2018, with early adoption

permitted as of the original eective date of January 1, 2017.

PG&E Corporation and the Utility are currently evaluating

the impact the guidance will have on their consolidated

financial statements and related disclosures.

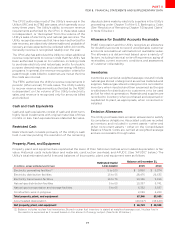

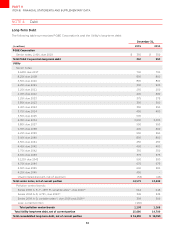

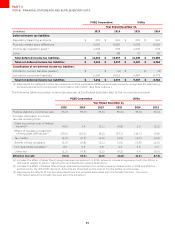

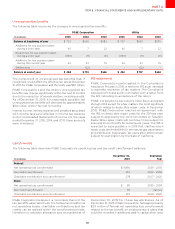

NOTE 3: Regulatory Assets, Liabilities, and Balancing Accounts

Regulatory Assets

Long-term regulatory assets are comprised of the following:

(inmillions)

BalanceatDecember Recovery

Period

Pensionbenefits() Indefinitely()

Deferredincometaxes() years

Utilityretainedgeneration() years

Environmentalcompliancecosts() years

Priceriskmanagement() years

Electromechanicalmeters() --

Unamortizedlossnetofgainonreacquireddebt() years

Other Various

Totallong-termregulatoryassets

() Representsthecumulativedifferencesbetweenamountsrecognizedforratemakingpurposesandexpenseoraccumulated

othercomprehensiveincome(loss)recognizedinaccordancewithGAAP

() InconnectionwiththesettlementagreemententeredintoamongPG&ECorporationtheUtilityandtheCPUCinto

resolvetheUtility’sproceedingunderChaptertheCPUCauthorizedtheUtilitytorecoverbillionofcostsrelated

totheUtility’sretainedgenerationassetsTheindividualcomponentsoftheseregulatoryassetsarebeingamortizedover

therespectivelivesoftheunderlyinggenerationfacilitiesconsistentwiththeperiodoverwhichtherelatedrevenuesare

recognized

() Representstheexpectedfuturerecoveryofthenetbookvalueofelectromechanicalmetersthatwerereplacedwith

SmartMeter™devicesAsofDecembertheremainingbalanceofmillionisincludedincurrentregulatoryassets

ontheConsolidatedBalanceSheets

() PaymentsintothepensionandotherbenefitsplansarebasedonannualcontributionrequirementsAstheseannual

requirementscontinueindefinitelyintothefuturetheUtilityexpectstocontinuouslyrecoverpensionbenefits

In general, the Utility does not earn a return on regulatory assets if the related costs do not accrue interest. Accordingly,

the Utility earns a return only on its regulatory assets for retained generation, regulatory assets for electromechanical

meters, and regulatory assets for unamortized loss, net of gain, on reacquired debt.