Pfizer 2013 Annual Report Download - page 5

Download and view the complete annual report

Please find page 5 of the 2013 Pfizer annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

|

|

Financial Review

Pfizer Inc. and Subsidiary Companies

4

2013 Financial Report

Specifically:

Recent Losses of Product Exclusivity Impacting Product Revenues

• Lipitor has lost exclusivity in all major markets. Lipitor revenues were $2.3 billion in 2013, $3.9 billion in 2012 and $9.6 billion in 2011. We

lost exclusivity for Lipitor in the U.S. in November 2011. The entry of multi-source generic competition in the U.S. began in May 2012, with

attendant increased competitive pressures. Lipitor lost exclusivity in Japan in June 2011, Australia in April 2012 and most of developed

Europe in March and May 2012 and now faces multi-source generic competition in those markets.

Prior to loss of exclusivity, sales of Lipitor in each market, except for those in Emerging Markets, were reported in our Primary Care

business unit. Typically, as of the beginning of the fiscal year following loss of exclusivity in a market, sales of Lipitor in that market, except

for those in Emerging Markets, were reported in our Established Products business unit. Sales of Lipitor in the U.S. and Japan have been

reported in our Established Products business unit since January 1, 2012, and sales of Lipitor in developed Europe have been reported in

our Established Products business unit since January 1, 2013.

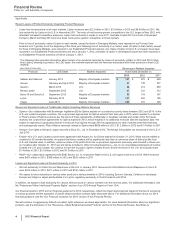

The following table provides information about certain of our products impacted by losses of exclusivity (LOEs) in 2013 and 2012 (other

than Lipitor), showing, by product, the LOE dates, the markets impacted and the revenues associated with those products in those LOE

markets:

(MILLIONS OF DOLLARS) Revenues in Markets Impacted

Products LOE Dates Markets Impacted Year Ended December 31,

2013 2012 2011

Xalatan and Xalacom January 2012 Majority of European markets $161 $275 $509

Aricept February and April 2012 Majority of European markets 47 139 347

Geodon March 2012 U.S. 84 214 859

Revatio tablet September 2012 U.S. 67 312 312

Detrol IR and Detrol LA September 2012 Majority of European markets 53 119 157

Lyrica February 2013 Canada 101 206 185

Viagra June 2013 Majority of European markets 265 370 400

Recent and Expected Losses of Collaboration Rights Impacting Alliance Revenues

• Spiriva—Our collaboration with Boehringer Ingelheim (BI) for Spiriva expires on a country-by-country basis between 2012 and 2016. In the

U.S. and certain European countries, the co-promotion agreements for Spiriva entered their final year in 2013, which resulted in a decline

in Pfizer’s share of Spiriva revenues per the terms of those agreements. Additionally, in Australia, Canada and certain other European

markets, the co-promotion agreements for Spiriva expired in 2013, which resulted in no additional revenues after the expiration date. We

expect to experience a graduated decline in revenues from Spiriva through 2016 as agreements for other markets enter their final year

and subsequently expire. Pfizer Alliance revenues related to Spiriva were $689 million in 2013, $1.2 billion in 2012 and $1.4 billion in 2011.

• Aricept—Our rights to Aricept in Japan returned to Eisai Co., Ltd. in December 2012. The Aricept 23mg tablet lost exclusivity in the U.S. in

July 2013.

• Enbrel—Our U.S. and Canada co-promotion agreement with Amgen Inc. for Enbrel expired on October 31, 2013. While we are entitled to

royalties for 36 months thereafter, we expect that those royalties will be significantly less than our previous share of Enbrel profits from

U.S. and Canada sales. In addition, while our share of the profits from this co-promotion agreement previously was included in Revenues,

our royalties after October 31, 2013 are and will be included in Other (income)/deductions––net, in our consolidated statements of income.

Outside the U.S. and Canada, we continue to have the exclusive rights to market Enbrel. Enbrel revenues in the U.S. and Canada were

$1.4 billion in 2013, $1.5 billion in 2012 and $1.3 billion in 2011.

• Rebif—Our collaboration agreement with EMD Serono Inc. to co-promote Rebif in the U.S. will expire at the end of 2015. Rebif revenues

were $401 million in 2013, $399 million in 2012 and $320 million in 2011.

Losses and Expected Losses of Product Exclusivity in 2014

• We lost exclusivity for Detrol LA and Rapamune in the U.S. in January 2014. Revenues for Detrol/Detrol LA and Rapamune in the U.S.

were $576 million in 2013, $671 million in 2012 and $745 million in 2011.

• We expect to lose exclusivity for various other products in various markets in 2014, including Zyvox in Canada, Celebrex in developed

Europe and Viagra in Japan and Australia. For Lyrica, regulatory exclusivity in the EU extends until 2014.

In addition, we expect to lose exclusivity for various other products in various markets over the next few years. For additional information, see

the “Patents and Other Intellectual Property Rights” section of our 2013 Annual Report on Form 10-K.

Our financial results in 2013 and our financial guidance for 2014, respectively, reflect the impact and projected impact of the loss of exclusivity

of various products and the expiration of certain alliance product contract rights discussed above. For additional information about our 2014

financial guidance, see the “Our Financial Guidance for 2014” section of this Financial Review.

We will continue to aggressively defend our patent rights whenever we deem appropriate. For more detailed information about our significant

products, see the discussion in the “Revenues––Major Biopharmaceutical Products” section of this Financial Review. See Notes to