Samsung 1999 Annual Report Download - page 50

Download and view the complete annual report

Please find page 50 of the 1999 Samsung annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

|

|

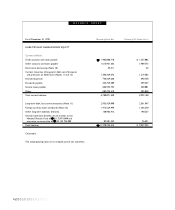

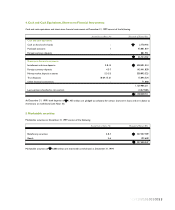

Cash, Cash Equivalents and Short-term Financial Instruments -

Cash and cash equivalents include cash on hand and in bank

accounts, with original maturities of three months or less.

Investments which are readily convertible into cash within four

to twelve months of purchase are classified in the balance

sheet as short-term financial instruments. The cost of these

investments approximates fair value.

Marketable Securities -

Marketable securities are stated at fair value.

Allowance for Doubtful Accounts -

The Company provides an allowance for doubtful accounts

and notes receivable based on the aggregate estimated

collectibility of the receivables.

Inventory Valuation -

Inventories are stated at the lower of cost or market, cost

being determined by the average cost method, except for

materials in transit which are stated at actual cost as

determined by the specific identification method.

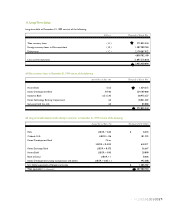

Property, Plant and Equipment and Related Depreciation -

Property, plant and equipment are stated at cost, except for

certain assets subject to upward revaluation in accordance

with the Asset Revaluation Law of Korea. The revaluation

presents production facilities and other buildings at their

depreciated replacement cost, and land at the prevailing

market price, as of the effective date of revaluation. The

revaluation increment, net of revaluation tax, is first applied to

offset accumulated deficit and deferred foreign exchange

losses, if any. The remainder may be credited to other capital

surplus or transferred to common stock. A new basis for

calculating depreciation is established for revalued assets (see

Note 8).

Depreciation is computed using the straight-line method,

based on the estimated useful lives of the assets as described

below.

Estimated

Useful Lives in Years

Buildings and auxiliary facilities 7 - 60

Machinery and equipment 2 - 10

Tools and fixtures 2 - 10

Structures and others 2 - 40

The Company capitalizes interest expense incurred on

borrowings used to finance the cost of constructing facilities

and equipment (see Note 8).

Maintenance and Repairs -

Routine maintenance and repairs are charged to expense as

incurred. Expenditures which enhance the value or extend the

useful life of the related assets are capitalized.

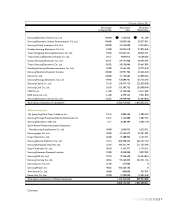

Equity Investments in Subsidiaries and Affiliated Companies &

Other Investments -

All investments in equity and debt securities are initially

carried at cost, including incidental expenses. The subsequent

accounting for investments by the type of security is as

follows.

Investments in marketable equity securities of non-controlled

investees, classified as other investments, are carried at fair

value. Temporary changes in fair value are accounted for in the

capital adjustment account, a component of stockholders'

equity. Declines in fair value which are anticipated to be

permanent are recorded in current operations after

eliminating any previously recorded capital adjustment for

temporary changes. Subsequent recoveries or other future

changes in fair value are recorded in the capital adjustment

account.

Investments in non-marketable equity securities of non-

controlled investees, classified as other investments, are

carried at cost, except for declines in the Company’s

proportionate ownership of the underlying book value of the

invested company which are anticipated to be permanent,

which are recorded in current operations. Subsequent

recoveries are also recorded in current operations up to the

original cost of the investments.

Investments in equity securities of companies over which the

Company exerts significant control or influence, classified as

equity investments in subsidiaries and affiliated companies, are

recorded using the equity method of accounting. Differences

between the initial purchase price and the Company's initial

proportionate ownership of the net book value of the invested

company are amortized over 5 years using the straight-line

method. Under the equity method, the Company records

changes in its proportionate ownership of the book value of

the invested company as current operations, capital

adjustments or adjustments to retained earnings, depending on

the nature of the underlying change in book value of the

invested company.

50001010010100101