US Postal Service 2012 Annual Report Download - page 88

Download and view the complete annual report

Please find page 88 of the 2012 US Postal Service annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

|

|

2012 Report on Form 10-K United States Postal Service- 87 -

RECLASSIFICATIONS

Certain prior year amounts related to short-term and long-term annual leave liabilities have been

reclassified to conform to the current year’s presentation. These reclassifications had no effect on

previously reported operating losses and net losses.

RELATED PARTIES

The Postal Service has significant transactions with other U.S. Government agencies, as disclosed

throughout this report. In addition to those amounts disclosed elsewhere, deferred revenue of $27 million for

2012 and $39 million for 2011 related to government deposits, is included in the Balance Sheets in

“Customer Deposit Accounts.”

CASH AND CASH EQUIVALENTS

Securities that mature within 90 days from the purchase date are deemed to be cash equivalents.

Included in “Cash and Cash Equivalents” are funds designated to be used for law enforcement purposes

and consumer fraud prevention awareness. The amounts so designated at the end of 2012 and 2011 were

$194 million and $169 million, respectively.

RECEIVABLES AND ALLOWANCE FOR DOUBTFUL ACCOUNTS

Receivables are carried at book value. Billed receivables are generally liquidated within one year and do not

have a stated interest rate.

Provision is made for doubtful accounts on outstanding receivables based on historical collection

experience and an estimate of uncollectible accounts as of the reporting date. The following summarizes

activity in the allowance for doubtful accounts:

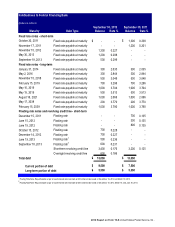

Allowance for Doubtful Accounts

(Dollars in millions)

Beginning Balance $ 37 $ 32 $ 29

Provision for Doubtful Accounts

11

13

11

Write-offs (7) (8) (8)

September 30 Balance $ 41 $ 37 $ 32

2012

2011

2010

PROPERTY AND EQUIPMENT

Property and equipment is stated at cost, including interest paid on funds borrowed to pay for the

construction of major capital additions, less accumulated depreciation. Property and equipment are

depreciated, using the straight-line method, over estimated useful lives, which range from 3 to 40 years,

except for buildings with historic status, which are depreciated over 75 years. See Note 5, Property and

Equipment for detailed information regarding Property and Equipment.

Leasehold improvements are amortized over the period of the lease or the useful life of the improvement,

whichever is shorter. Leasehold improvements that are placed in service after the start of the lease term

are amortized over the shorter of the useful life of the asset or the remaining lease term, including renewal

options that are reasonably assured to be executed.

The depreciation and amortization of capital assets over estimated useful lives require management to

make judgments about future events. Capital assets are utilized over relatively long periods of time;

therefore, periodic evaluations of whether adjustments to the estimated service lives are necessary to

ensure that these estimates properly match the economic useful lives of the assets.