Bank of America 2001 Annual Report Download - page 88

Download and view the complete annual report

Please find page 88 of the 2001 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

|

|

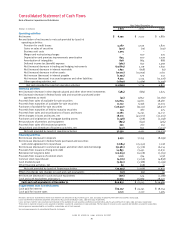

BANK OF AMERICA 2001 ANNUAL REPORT

86

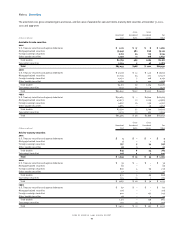

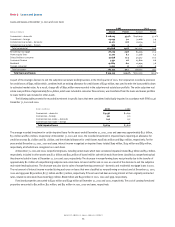

The Corporation allocated the total cost of mortgage loans originated for sale or purchased between the cost of the loans, and when applicable,

the Certificates and the mortgage servicing rights (MSR) based on the relative fair values of the loans, the Certificates and the MSR. MSR acquired

separately are capitalized at cost. The Corporation capitalized $1.1 billion, $836 million and $1.6 billion of MBA during 2001, 2000 and 1999, respec-

tively. The cost of MSR was amortized in proportion to and over the estimated period that servicing revenues were recognized. Amortization was

$540 million and $566 million during 2000 and 1999, respectively. The fair value of capitalized MSR was $3.8 billion at December 31, 2000.

Mortgage banking income includes servicing fees, gains from selling originated mortgages, ancillary servicing income, mortgage production

fees, gains and losses on sales to the secondary market, and income on the Certificates.

Goodwill and Other Intangibles

Net assets of companies acquired in purchase transactions are recorded at fair value at the date of acquisition. Identified intangibles are amortized

on an accelerated or straight-line basis over the period benefited. Goodwill is amortized on a straight-line basis over a period not to exceed 25 years.

The recoverability of goodwill and other intangibles is evaluated if events or circumstances indicate a possible impairment. Such evaluation is based

on various analyses, including undiscounted cash flow projections. See “Recently Issued Accounting Pronouncements” on page 82 for information

related to changes in accounting for goodwill and other intangibles which were effective January 1, 2002.

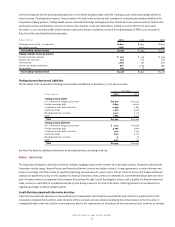

Off-Balance Sheet Financing Entities

In the ordinary course of business, the Corporation supports its customers financing needs by facilitating these customers’ access to different funding

sources, assets and risks. In addition, the Corporation utilizes certain financing arrangements to meet its balance sheet management, funding, liquidity,

and market or credit risk management needs. These financing entities may be in the form of corporations, partnerships or limited liability companies,

or trusts and are not consolidated in the Corporation’s balance sheet. The majority of these activities are basic term or revolving securitization vehicles.

These vehicles are generally funded through term-amortizing debt structures designed to be paid off based on the underlying cash flows of the assets

securitized. Other, lesser used vehicles, are generally funded with short-term commercial paper and are similarly paid down through the cash flow or sale

of the underlying assets. Securitization activities are further discussed in more detail in the Securitizations section below and Note Eight.

These financing entities are usually contractually limited to a narrow range of activities that facilitate the transfer of or access to various types of

assets or financial instruments. In certain situations, the Corporation provides liquidity commitments and/or loss protection agreements. See Note

Twelve for further discussion.

The Corporation evaluates whether these entities should be consolidated by applying various generally accepted accounting principles and

interpretations that generally provide that a financing entity is not consolidated if both the control and risks and rewards of the assets in the financing

entity are not retained by the Corporation. In determining whether the financing entity should be consolidated, the Corporation considers whether the

entity is a qualifying special-purpose entity (QSPE) as defined in SFAS 140. For non-consolidation, SFAS 140 requires that the financing entity be

legally isolated, bankruptcy remote and beyond the control of the seller, which generally applies to securitizations. For non-securitization structures,

the Securities and Exchange Commission and the Emerging Issues Task Force also have issued guidance regarding consolidation of financing entities.

Such guidance applies to certain transactions and requires an assessment of whether sufficient risks and rewards of ownership have passed based

on assessing the voting rights, control of the entity and the existence of substantive third party equity investment.

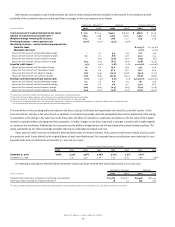

Securitizations

The Corporation securitizes, sells and services interests in residential mortgage, consumer finance, commercial and bankcard loans. When the Corporation

securitizes assets, it may retain interest-only strips, one or more subordinated tranches and, in some cases, a cash reserve account, all of which are

considered retained interests in the securitized assets. Gains upon sale of the assets depend, in part, on the Corporation’s allocation of the previous

carrying amount of the assets to the retained interests. Previous carrying amounts are allocated in proportion to the relative fair values of the assets

sold and interests retained.

Quoted market prices, if available, are used to obtain fair values. Generally, quoted market prices for retained interests are not available; therefore,

the Corporation estimates fair values based upon the present value of the associated expected future cash flows. This requires management to estimate

credit losses, prepayment speeds, forward yield curves, discount rates and other factors that impact the value of retained interests.

The excess cash flows expected to be received over the amortized cost of the retained interest is recognized as interest income using the effective

yield method. If the fair value of the retained interest has declined below its carrying amount and there has been an adverse change in estimated

cash flows (as defined), then such decline is determined to be other-than-temporary and the retained interest is written down to fair value with a

corresponding adjustment to earnings.