Berkshire Hathaway 2005 Annual Report Download - page 10

Download and view the complete annual report

Please find page 10 of the 2005 Berkshire Hathaway annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

|

|

The Public Utility Holding Company Act (“PUHCA”) was repealed on August 8, 2005, a

milestone that allowed Berkshire to convert its MidAmerican preferred stock into voting common shares on

February 9, 2006. This conversion ended a convoluted corporate arrangement that PUHCA had forced

upon us. Now we have 83.4% of both the common stock and the votes at MidAmerican, which allows us

to consolidate the company’ s income for financial accounting and tax purposes. Our true economic

interest, however, is the aforementioned 80.5%, since there are options outstanding that are sure to be

exercised within a few years and that upon exercise will dilute our ownership.

Though our voting power has increased dramatically, the dynamics of our four-party ownership

have not changed at all. We view MidAmerican as a partnership among Berkshire, Walter Scott, and two

terrific managers, Dave Sokol and Greg Abel. It’ s unimportant how many votes each party has; we will

make major moves only when we are unanimous in thinking them wise. Five years of working with Dave,

Greg and Walter have underscored my original belief: Berkshire couldn’ t have better partners.

You will notice that this year we have provided you with two balance sheets, one representing our

actual figures per GAAP on December 31, 2005 (which does not consolidate MidAmerican) and one that

reflects the subsequent conversion of our preferred. All future financial reports of Berkshire will include

MidAmerican’ s figures.

Somewhat incongruously, MidAmerican owns the second largest real estate brokerage firm in the

U.S. And it’ s a gem. The parent company’ s name is HomeServices of America, but our 19,200 agents

operate through 18 locally-branded firms. Aided by three small acquisitions, we participated in $64 billion

of transactions last year, up 6.5% from 2004.

Currently, the white-hot market in residential real estate of recent years is cooling down, and that

should lead to additional acquisition possibilities for us. Both we and Ron Peltier, the company’ s CEO,

expect HomeServices to be far larger a decade from now.

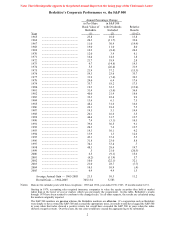

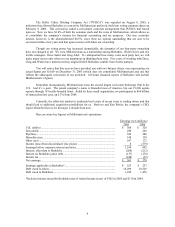

Here are some key figures on MidAmerican’ s operations:

Earnings (in $ millions)

2005 2004

U.K. utilities ....................................................................................................... $ 308 $ 326

Iowa utility ......................................................................................................... 288 268

Pipelines ............................................................................................................. 309 288

HomeServices..................................................................................................... 148 130

Other (net) .......................................................................................................... 107 172

Income (loss) from discontinued zinc project .................................................... 8 (579)

Earnings before corporate interest and taxes ...................................................... 1,168 605

Interest, other than to Berkshire ......................................................................... (200) (212)

Interest on Berkshire junior debt ........................................................................ (157) (170)

Income tax .......................................................................................................... (248) (53)

Net earnings........................................................................................................ $ 563 $ 170

Earnings applicable to Berkshire*...................................................................... $ 523 $ 237

Debt owed to others............................................................................................ 10,296 10,528

Debt owed to Berkshire...................................................................................... 1,289 1,478

*Includes interest earned by Berkshire (net of related income taxes) of $102 in 2005 and $110 in 2004.

9