Pfizer 2008 Annual Report Download - page 14

Download and view the complete annual report

Please find page 14 of the 2008 Pfizer annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

|

|

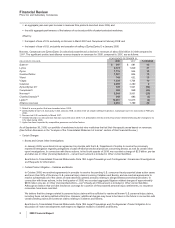

Financial Review

Pfizer Inc and Subsidiary Companies

•In June 2006, we entered into a license agreement with Bayer Pharmaceuticals Corporation to acquire exclusive worldwide rights to

DGAT-1 inhibitors.

•In June 2006, we acquired the worldwide rights to Toviaz (fesoterodine), a drug for treating overactive bladder which was approved in

the E.U. in April 2007 and in the U.S. in October 2008, from Schwarz Pharma AG.

•In March 2006, we entered into research collaborations with NicOX SA in ophthalmic disorders and NOXXON Pharma AG in

Alzheimer’s disease and ophthalmic disorders.

•In February 2006, we completed the acquisition of the sanofi-aventis worldwide rights, including patent rights and production

technology, to manufacture and sell Exubera, an inhaled form of insulin, and the insulin-production business and facilities located in

Frankfurt, Germany, previously jointly owned by Pfizer and sanofi-aventis, for approximately $1.4 billion in cash (including transaction

costs). Substantially all assets recorded in connection with this acquisition have now been written off. (See the “Our 2008 Performance:

Certain Charges—Exubera” section of this Financial Review.) Prior to the acquisition, in connection with our collaboration agreement

with sanofi-aventis, we recorded a research and development milestone due to us from sanofi-aventis of approximately $118 million

($71 million, after tax) in 2006 in Research and development expenses upon the approval of Exubera in January 2006 by the FDA.

•In December 2006, we completed the acquisition of PowderMed, a U.K. company which specializes in the emerging science of

DNA-based vaccines for the treatment of influenza and chronic viral diseases, and in May 2006, we completed the acquisition of Rinat,

a biologics company with several new central-nervous-system product candidates. In 2006, the aggregate cost of these and other

smaller acquisitions was approximately $880 million (including transaction costs). In connection with these transactions, we recorded

$835 million in Acquisition-related in-process research and development charges.

Dispositions

We evaluate our businesses and product lines periodically for strategic fit within our operations.

In the fourth quarter of 2006, we sold our Consumer Healthcare business for $16.6 billion, and recorded a gain of approximately

$10.2 billion ($7.9 billion, net of tax) in Gains on sales of discontinued operations—net of tax in the consolidated statement of

income for 2006. In 2007, we recorded a loss of approximately $70 million, after-tax, primarily related to the resolution of

contingencies, such as purchase price adjustments and product warranty obligations, as well as pension settlements. This business

was composed of:

•substantially all of our former Consumer Healthcare segment;

•other associated amounts, such as purchase-accounting impacts, acquisition-related costs and restructuring and implementation costs

related to our cost-reduction initiatives that were previously reported in the Corporate/Other segment; and

•certain manufacturing facility assets and liabilities, which were previously part of our Pharmaceutical or Corporate/Other segment but

were included in the sale of the Consumer Healthcare business. The net impact to the Pharmaceutical segment was not significant.

The results of this business are included in Income from discontinued operations—net of tax for 2006. (See Notes to Consolidated

Financial Statements—Note 3. Discontinued Operations.)

We continued during 2008 and 2007, and will continue for a period of time, to generate cash flows and to report income statement

activity in continuing operations that are associated with our former Consumer Healthcare business. The activities that give rise to

these impacts are transitional in nature and generally result from agreements that ensure and facilitate the orderly transfer of

business operations to the new owner. Included in continuing operations for 2008 and 2007 were the following amounts associated

with these transition service agreements that will no longer occur after the full transfer of activities to the new owner: for 2008,

Revenues of $172 million; Cost of sales of $162 million; and Selling, informational and administrative expenses of $3 million and for

2007, Revenues of $219 million; Cost of sales of $194 million; Selling, informational and administrative expenses of $15 million; and

Other (income)/deductions—net of $16 million in income.

Our Expectations for 2009

While our revenues and income will continue to be tempered in the near term due to patent expirations and other factors, we will

continue to make the investments necessary to sustain long-term growth. We remain confident that Pfizer has the organizational

strength and resilience, as well as the strategies, the financial depth and flexibility, to succeed in the long term. However, no

assurance can be given that the factors described above under “Our Operating Environment and Response to Key Opportunities

and Challenges” or below under “Forward-Looking Information and Factors That May Affect Future Results” or other significant

factors will not have a material adverse effect on our business and financial results.

Compared to 2008, our 2009 guidance, at current exchange rates, reflects increased pension expenses, lower interest income, as

well as an increase in the effective tax rate resulting from financial strategies in connection with our proposed acquisition of Wyeth.

At current exchange rates, we forecast 2009 revenues of $44.0 billion to $46.0 billion, reported diluted earnings per common share

(EPS) of $1.34 to $1.49 and Adjusted diluted EPS of $1.85 to $1.95. On January 26, 2009, we announced the implementation of a

new cost-reduction initiative that we anticipate will achieve a reduction in adjusted total costs of approximately $3 billion, on a

constant currency basis, by the end of 2011, compared with our 2008 adjusted total costs. We plan to reinvest approximately $1

12 2008 Financial Report