Western Digital 2008 Annual Report Download - page 4

Download and view the complete annual report

Please find page 4 of the 2008 Western Digital annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

|

|

This is a great time to be in the growing global hard drive industry.

Storage demand and applications for hard drives continue to

proliferate in computing and consumer markets as both workplace

and lifestyle changes generate massive volumes of data to be

secured conveniently and cost effectively on hard drives.

• In fi scal 2008 the HDD market generated revenues in excess

of $35 billion with 540 million hard drives shipped, while

forecasted demand for fi scal 2009 exceeds 620 million units.

• On a unit basis, the overall hard drive market is looking at

a fi ve-year CAGR of approximately 13 percent, while those

markets served by WD are forecast to grow in excess of

16 percent annually.

• The industry’s fastest growth opportunities continue to be in the

notebook PC and branded product markets, areas of continued

emphasis for WD.

While maintaining our focus on the high-volume desktop PC

market, we remain committed to our multi-year diversifi cation

effort. As a result, hard drive revenues from non-desktop markets

expanded to 56 percent of revenue in fi scal 2008, compared with

43 percent in fi scal 2007 and 29 percent in fi scal 2006. More

specifi cally:

• We saw tremendous growth this year in the 2.5-inch notebook

PC and branded products markets:

° We tripled our 2.5-inch drive shipments, year-over-year, to

37 million units and with continued new product execution,

we are well positioned for continued growth and market

expansion in this space.

° We increased sales of our branded products by 60 percent

year-over-year to $1.4 billion and we continued to add new

products and product features to the line up, to strengthen

our leadership position in the external storage space and

expand our available market.

• At the same time we made good strides in other non-traditional

markets such as Serial ATA (SATA) drives for the enterprise

space and 3.5-inch drives for consumer electronics (CE).

° In Enterprise SATA, a fast growing portion of the enterprise

storage market, we continued to innovate with the

introduction of our 3.5-inch WD RE2-GP SATA drives with

GreenPower™ technology and the WD VelociRaptor™ drive

family, the industry’s fi rst 300 gigabyte (GB) 10,000 RPM,

2.5-inch drive.

° In CE, the introduction of our power-saving GreenPower™

technology to our WD AV hard drives, combined with

improved costs and our demonstrated fi eld quality

performance, led to enhanced value for our customers and

improved contribution to WD’s business.

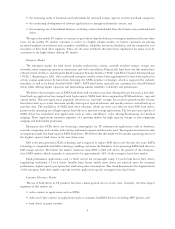

CAPITAL EXPENDITURES, RESEARCH

and DEVELOPMENT SPENDING

$434

$565 $630

$334

$0

$200

$400

$600

$800

$1,000

$1,200

FY2004 FY2005 FY2006 FY2007 FY2008

Dollars in millions

$1,079

Fiscal 2008 represented our sixth consecutive year of

substantial growth in our research and development

and capital spending to support a signifi cant deepening

and acceleration of our technology capability and

broadening of our product portfolio.

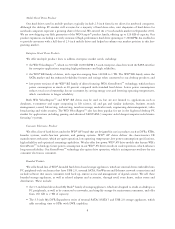

*Revenue percentages are based on sales of hard drives only.

REVENUE DIVERSIFICATION*

86%

14%

79%

21%

71%

29%

57%

43%

44%

56%

$8,000

$9,000

$7,000

$6,000

$5,000

$4,000

$3,000

$2,000

$1,000

$0

FY2004 FY2005 FY2006 FY2007 FY2008

Desktop Revenue

Non-Desktop Revenue

$3,047

$3,639 $4,341

$5,468

$8,074

Dollars in millions

While maintaining our focus in the high-volume

desktop market, we have made major strides in

diversifying the business, by establishing our

footprint in newer, faster-growth markets. As a result,

we saw our hard drive revenue from non-desktop

markets expand to 56% in fi scal 2008.

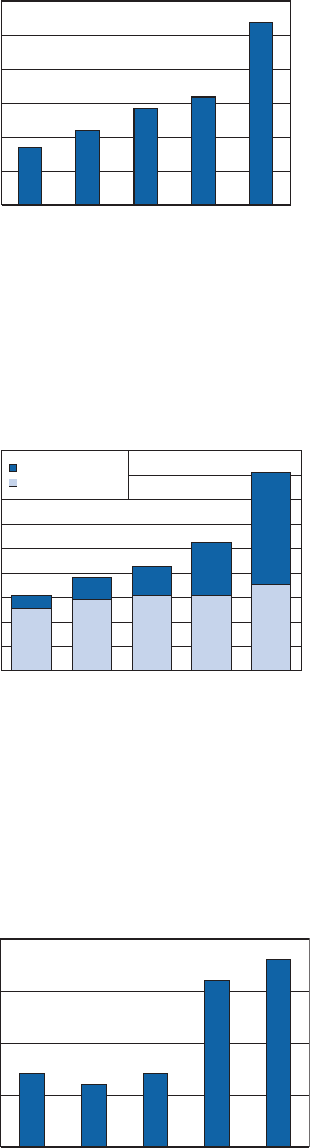

PERCENTAGE OF REVENUE

FROM BRANDED PRODUCTS*

7% 6% 7%

16%

18%

0%

5%

10%

15%

20%

FY2004 FY2005 FY2006 FY2007 FY2008

*Based on sales of hard drives only.

Our branded products revenue grew to 18% of

total revenue, up from 16% in fi scal 2007, refl ecting

growing demand for safe and secure external

storage and for the My Book® and My Passport™

product families.