3M 2013 Annual Report Download - page 79

Download and view the complete annual report

Please find page 79 of the 2013 3M annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

|

|

73

3M reviews impairments associated with its marketable securities in accordance with the measurement guidance provided

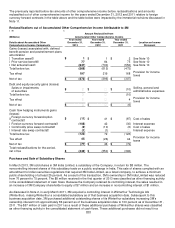

by ASC 320, Investments-Debt and Equity Securities, when determining the classification of the impairment as

“temporary” or “other-than-temporary”. A temporary impairment charge results in an unrealized loss being recorded in the

other comprehensive income component of shareholders’ equity. Such an unrealized loss does not reduce net income

attributable to 3M for the applicable accounting period because the loss is not viewed as other-than-temporary. The

factors evaluated to differentiate between temporary and other-than-temporary include the projected future cash flows,

credit ratings actions, and assessment of the credit quality of the underlying collateral, as well as other factors.

The balance at December 31, 2013 for marketable securities by contractual maturity are shown below. Actual maturities

may differ from contractual maturities because the issuers of the securities may have the right to prepay obligations

without prepayment penalties.

(Millions)

December 31, 2013

Due in one year or less $

287

Due after one year through five years 1,898

Due after five years through ten years 24

Due after ten years ―

Total marketable securities $

2,209

3M has a diversified marketable securities portfolio of $2.209 billion as of December 31, 2013. Within this portfolio, current

and long-term asset-backed securities (estimated fair value of $907 million) primarily include interests in automobile loans,

credit cards and equipment leases. 3M’s investment policy allows investments in asset-backed securities with minimum

credit ratings of Aa2 by Moody’s or AA by S&P or Fitch. At December 31, 2013, all asset-backed security investments

were in compliance with this policy. Approximately 98.1 percent of all asset-backed security investments were rated AAA

or A-1+ by Standard & Poor’s and/or Aaa or P-1 by Moody’s Investors Service and/or AAA or F1+ by Fitch Ratings.

3M’s marketable securities portfolio includes auction rate securities that represent interests in investment grade credit

default swaps; however, currently these holdings comprise less than one percent of this portfolio. The estimated fair value

of auction rate securities are $11 million and $7 million as of December 31, 2013 and 2012, respectively. Gross unrealized

losses within accumulated other comprehensive income related to auction rate securities totaled $2 million (pre-tax) and

$6 million (pre-tax) as of December 31, 2013 and 2012, respectively. As of December 31, 2013, auction rate securities

associated with these balances have been in a loss position for more than 12 months. Since the second half of 2007,

these auction rate securities failed to auction due to sell orders exceeding buy orders. Liquidity for these auction-rate

securities is typically provided by an auction process that resets the applicable interest rate at pre-determined intervals,

usually every 7, 28, 35, or 90 days. The funds associated with failed auctions will not be accessible until a successful

auction occurs or a buyer is found outside of the auction process. Refer to Note 12 for a table that reconciles the

beginning and ending balances of auction rate securities.