AT&T Wireless 2009 Annual Report Download - page 77

Download and view the complete annual report

Please find page 77 of the 2009 AT&T Wireless annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

|

|

AT&T 09 AR 75

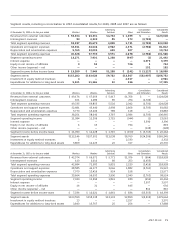

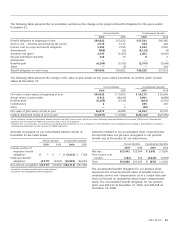

failure by AT&T or any subsidiary to pay when due other

debt above a threshold amount that results in acceleration

of that debt (commonly referred to as “cross-acceleration”)

or commencement by a creditor of enforcement proceedings

within a specified period after a monetary judgment above

a threshold amount has become final; acquisition by any

person of beneficial ownership of more than 50% of AT&T

common shares or a change of more than a majority of

AT&T’s directors in any 24-month period other than as

elected by the remaining directors (commonly referred to as

a “change-in-control”); material breaches of representations

in the agreement; failure to comply with the negative pledge

or debt-to-EBITDA ratio covenants described above; failure

to comply with other covenants for a specified period after

notice; failure by AT&T or certain affiliates to make certain

minimum funding payments under Employee Retirement

Income Security Act of 1974, as amended (ERISA); and

specified events of bankruptcy or insolvency.

NOTE 9. FAIR VALUE MEASUREMENTS AND DISCLOSURE

GAAP standards require disclosures for financial assets and

liabilities that are remeasured at fair value at least annually.

GAAP standards establish a three-tier fair value hierarchy,

which prioritizes the inputs used in measuring fair value.

The Fair Value Measurement and Disclosure framework

provides a fair value hierarchy that prioritizes the inputs to

valuation techniques used to measure fair value. The hierarchy

gives the highest priority to unadjusted quoted prices in

active markets for identical assets or liabilities (Level 1

measurements) and the lowest priority to unobservable

inputs (Level 3 measurements). The three levels of the fair

value hierarchy under Fair Value Measurement and

Disclosure are described below:

Credit Facility We have a five-year credit agreement with a

syndicate of investment and commercial banks. In June 2009,

one of the participating banks, Lehman Brothers Bank, Inc.,

which had declared bankruptcy, terminated its lending

commitment of $535 and withdrew from the agreement.

As a result of this termination, the outstanding commitments

under the agreement were reduced from a total of $10,000

to $9,465. We still have the right to increase commitments

up to an additional $2,535 provided no event of default under

the credit agreement has occurred. The current agreement

will expire in July 2011. We also have the right to terminate,

in whole or in part, amounts committed by the lenders

under this agreement in excess of any outstanding advances;

however, any such terminated commitments may not be

reinstated. Advances under this agreement may be used for

general corporate purposes, including support of commercial

paper borrowings and other short-term borrowings.

There is no material adverse change provision governing

the drawdown of advances under this credit agreement.

This agreement contains a negative pledge covenant,

which requires that, if at any time we or a subsidiary pledges

assets or otherwise permits a lien on its properties, advances

under this agreement will be ratably secured, subject to

specified exceptions. We must maintain a debt-to-EBITDA

(earnings before interest, income taxes, depreciation and

amortization, and other modifications described in the

agreement) financial ratio covenant of not more than

three-to-one as of the last day of each fiscal quarter for

the four quarters then ended. We comply with all covenants

under the agreement. At December 31, 2009, we had no

borrowings outstanding under this agreement.

Defaults under the agreement, which would permit the

lenders to accelerate required payment, include nonpayment

of principal or interest beyond any applicable grace period;

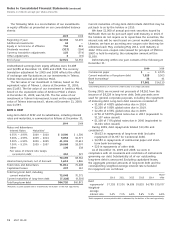

LEVEL 1 Inputs to the valuation methodology are unadjusted quoted prices for identical assets or liabilities in active markets

that AT&T has the ability to access.

LEVEL 2 Inputs to the valuation methodology include:

• Quotedpricesforsimilarassetsandliabilitiesinactivemarkets;

• Quotedpricesforidenticalorsimilarassetsorliabilitiesininactivemarkets;

• Inputsotherthanquotedmarketpricesthatareobservablefortheassetorliability;

• Inputsthatarederivedprincipallyfromorcorroboratedbyobservablemarketdatabycorrelationorothermeans.

If the asset or liability has a specified (contractual) term, the Level 2 input must be observable for substantially the

full term of the asset or liability.

LEVEL 3 Inputs to the valuation methodology are unobservable and significant to the fair value measurement.

• Fairvalueisoftenbasedoninternallydevelopedmodelsinwhichtherearefew,ifany,externalobservations.