Berkshire Hathaway 2009 Annual Report Download - page 15

Download and view the complete annual report

Please find page 15 of the 2009 Berkshire Hathaway annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

|

|

Last year I told you why our buyers – generally people with low incomes – performed so well as credit

risks. Their attitude was all-important: They signed up to live in the home, not resell or refinance it.

Consequently, our buyers usually took out loans with payments geared to their verified incomes (we weren’t

making “liar’s loans”) and looked forward to the day they could burn their mortgage. If they lost their jobs, had

health problems or got divorced, we could of course expect defaults. But they seldom walked away simply

because house values had fallen. Even today, though job-loss troubles have grown, Clayton’s delinquencies and

defaults remain reasonable and will not cause us significant problems.

We have tried to qualify more of our customers’ loans for treatment similar to those available on the

site-built product. So far we have had only token success. Many families with modest incomes but responsible

habits have therefore had to forego home ownership simply because the financing differential attached to the

factory-built product makes monthly payments too expensive. If qualifications aren’t broadened, so as to open

low-cost financing to all who meet down-payment and income standards, the manufactured-home industry seems

destined to struggle and dwindle.

Even under these conditions, I believe Clayton will operate profitably in coming years, though well

below its potential. We couldn’t have a better manager than CEO Kevin Clayton, who treats Berkshire’s interests

as if they were his own. Our product is first-class, inexpensive and constantly being improved. Moreover, we will

continue to use Berkshire’s credit to support Clayton’s mortgage program, convinced as we are of its soundness.

Even so, Berkshire can’t borrow at a rate approaching that available to government agencies. This handicap will

limit sales, hurting both Clayton and a multitude of worthy families who long for a low-cost home.

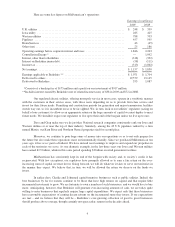

In the following table, Clayton’s earnings are net of the company’s payment to Berkshire for the use of

its credit. Offsetting this cost to Clayton is an identical amount of income credited to Berkshire’s finance

operation and included in “Other Income.” The cost and income amount was $116 million in 2009 and $92

million in 2008.

The table also illustrates how severely our furniture (CORT) and trailer (XTRA) leasing operations

have been hit by the recession. Though their competitive positions remain as strong as ever, we have yet to see

any bounce in these businesses.

Pre-Tax Earnings

(in millions)

2009 2008

Net investment income ....................................... $278 $330

Life and annuity operation .................................... 116 23

Leasing operations .......................................... 14 87

Manufactured-housing finance (Clayton) ........................ 187 206

Other income * ............................................. 186 141

Income before investment and derivatives gains or losses ........... $781 $787

*Includes $116 million in 2009 and $92 million in 2008 of fees that Berkshire charges Clayton for the

use of Berkshire’s credit.

************

At the end of 2009, we became a 50% owner of Berkadia Commercial Mortgage (formerly known as

Capmark), the country’s third-largest servicer of commercial mortgages. In addition to servicing a $235 billion

portfolio, the company is an important originator of mortgages, having 25 offices spread around the country.

Though commercial real estate will face major problems in the next few years, long-term opportunities for

Berkadia are significant.

13