Costco 2002 Annual Report Download - page 14

Download and view the complete annual report

Please find page 14 of the 2002 Costco annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

|

|

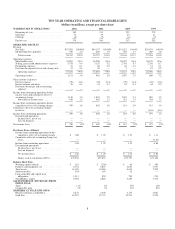

equipment for warehouse clubs and related operations; and approximately $100,000 to $150,000 for international

expansion, including the United Kingdom, Asia, Mexico and other potential ventures. These expenditures will be

financed with a combination of cash provided from operations, the use of cash and cash equivalents and short-

term investments, short-term borrowings under the Company’s commercial paper program, Senior Notes and

other financing sources as required.

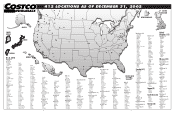

Expansion plans for the United States and Canada during fiscal 2003 are to open approximately 28 to 30

new warehouse clubs, including three to five relocations to larger and better-located warehouses. The Company

expects to continue expansion of its international operations and plans to open two additional warehouses in the

United Kingdom through its 80%-owned subsidiary, and two additional warehouses in Japan. Other international

markets are being assessed.

Costco and its Mexico-based joint venture partner, Controladora Comercial Mexicana, each own a 50% in-

terest in Costco Mexico. As of September 1, 2002, Costco Mexico operated 20 warehouses in Mexico and plans

to open one or two new warehouse clubs during fiscal 2003.

Reorganization of Canadian Administrative Operations

On January 17, 2001, the Company announced plans to reorganize and consolidate the administration of its

operations in Canada. Total costs related to the reorganization were $26,765 pre-tax, of which $7,765 pre-tax

($4,775 after-tax, or $.01 per diluted share) was expensed in fiscal 2002 and $19,000 pre-tax ($11,400 after-tax,

or $.02 per diluted share) was expensed in fiscal 2001 and reported as part of the provision for impaired assets

and closing costs. These costs consisted primarily of employee severance, implementation and consolidation of

support systems and employee relocation. The reorganization was completed in the first quarter of fiscal 2002.

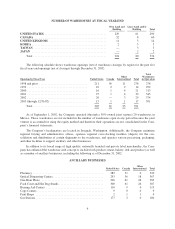

Bank Credit Facilities and Commercial Paper Programs (all amounts stated in thousands of US dollars)

The Company has in place a $500,000 commercial paper program supported by a $400,000 bank credit fa-

cility with a group of 10 banks, of which $200,000 expires on November 11, 2003 and $200,000 expires on

November 15, 2005. At September 1, 2002, no amounts were outstanding under the commercial paper program

and no amounts were outstanding under the credit facility.

In addition, a wholly owned Canadian subsidiary has a $128,000 commercial paper program supported by a

$51,000 bank credit facility with a group of three Canadian banks, which expires in March, 2003. At

September 1, 2002, no amounts were outstanding under the Canadian commercial paper program or the bank

credit facility. The Company is evaluating the business need to renew this commercial paper program and bank

credit facility.

The Company has agreed to limit the combined amount outstanding under the U.S. and Canadian commer-

cial paper programs to the $451,000 combined amounts of the respective supporting bank credit facilities.

The Company’s wholly-owned Japanese subsidiary has a short-term ¥4 billion bank line of credit, equal to

approximately $33,600, of which ¥1 billion ($8,400) expires in April 2003 and ¥3 billion ($25,200) expires in

November 2003. At September 1, 2002, $18,480 was outstanding under the line of credit with an applicable

interest rate of 1.375%.

The Company’s 80%-owned UK subsidiary has a £60 million ($93,048) bank revolving credit facility and a

£20 million ($31,016) bank overdraft facility, both expiring in February 2007. At September 1, 2002, $85,294

was outstanding under the revolving credit facility with an applicable interest rate of 4.413% and no balance was

outstanding under the bank overdraft facility.

13