Tesco 2007 Annual Report Download - page 13

Download and view the complete annual report

Please find page 13 of the 2007 Tesco annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

|

|

11

OPERATING AND

FINANCIAL REVIEW

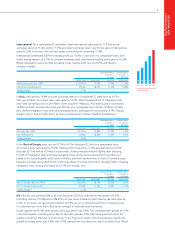

•Tesco Malaysia has made excellent progress, moving

strongly through to profitability in the year, delivering

another year of very strong (over 50%) sales growth, and

achieving a near-doubling of space helped by the Makro

acquisition, which completed in January. Substantial refits

to the Makro stores have now begun, taking eight to nine

weeks per store to complete and involving significant

changes to layouts and ranges. We are developing a

good market position in Malaysia with a strong new store

programme in place for this year which will add a further

22% of space to our network.

• Political uncertainty in Thailand during the second half of

the year produced a difficult business climate. Nevertheless,

Tesco Lotus, which has a strong market position, again

performed well, delivering good growth in sales and profit.

The successful development and roll-out of new small

formats continues and to date, we have 370 stores trading

across four formats, including 75 hypermarkets (of which

17 are Value stores). We also have 266 Express stores

and 29 supermarkets which are proving very popular

with customers.

Europe Our rate of expansion in European markets stepped up

significantly in the year with 4.7m sq ft of new space added –

representing almost 30% growth. Successful regional initiatives

to strengthen our business – from pan-European purchasing

of own brand products and fresh produce to the introduction

of the Cherokee clothing range – have contributed to further

improvements in our competitiveness. Customer numbers

are up significantly and this is driving substantial market

share gains.

• In the Czech Republic, our business has grown by almost

two-thirds in the year and is now one of the leaders in the

market. We again delivered strong profit growth despite

competitive market conditions and the challenges of

integrating the Carrefour and Edeka acquisitions.

Conversion of the 11 Carrefour stores is almost complete,

we have a strong organic store opening programme which

will add some 13% to our space in the current year and we

have begun remodelling our department stores – with the

first, at Brno, performing well.

• We continued to make progress in Hungary but although

overall sales grew, profit performance was below budget.

The effects of Government austerity measures last August

on an already difficult economic and retail environment

have been severe. Consumer spending levels are

significantly down, with non-food categories particularly

affected. Despite these challenges we have a strong

market position which we have continued to strengthen

by lowering prices, expanding our store network and

developing our infrastructure. We opened 14 new stores

in 2006/07, including 10 hypermarkets, and we plan

to add 15% to our total space in the current year.

• Against the background of an improving economy and a

consolidating retail industry in Poland, we are making very

good progress, with rising sales, profits and returns. Sales

growth has continued to be strong, driven by sustained

improvement in existing store performance and a growing

contribution from new space. The development of our

1k (around 10,000 sqft), 2k and 3k store formats as part

of an enlarged opening programme is going well. The

acquisition of the Leader Price stores from Casino, which

was announced last July and completed in December has

accelerated our 1k format expansion and contributed to a

37% overall space increase in Poland. Leader Price stores

are being converted rapidly to Tesco with, on average,

25% sales uplifts.

•Tesco

Ireland delivered another excellent performance with

improved profits and another year of strong sales growth

in existing stores. Our new store opening programme

will be substantially bigger this year – with 240,000 sq ft,

representing growth of over 10%. The new 740,000 sq ft

distribution centre at Donabate, in north Dublin, opens this

month. Our competitive position is also strong and we’re

investing more for customers – for example, our largest

ever programme of price cuts in Ireland, which started last

spring, has been well-received.

• In Slovakia the success of our compact hypermarket format

and a strong economy have underpinned pleasing growth

in sales, profits and returns. We now have 25 such stores,

representing approaching half of our total space, with more

planned. We introduced our 1k format this year – opening

the first store at Vrable and we now have six trading with

nine more planned this year. Our organic expansion will

add around 15% to our space this year.