Tesco 2008 Annual Report Download - page 8

Download and view the complete annual report

Please find page 8 of the 2008 Tesco annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

|

|

Tesco PLC Annual Report and

Financial Statements 2008

6

Joint ventures and associates Our share of profit (net of tax and

interest) for the year was £75m, a decrease of £31m compared with last

year. Driving this decrease was a £47m property profit last year, principally

reflecting profit realised on the sale of the Weston Favell store to a third

party. Excluding these property-related items, profits from joint ventures

rose by £16m.

Tesco Personal Finance (TPF) profit was £128m, of which our share was

£64m. This was after absorbing £31m of higher household insurance claims

linked to last summer’s flooding in Yorkshire and the Midlands. Tesco’s share

of the cost of higher claims linked to these events was £11m (after interest

and tax) in the year as a whole.

Underlying growth in the business was therefore encouraging, with the

new management team demonstrating that there remains significant

growth potential for TPF within the financial services sector, particularly

amongst loyal Tesco customers, as we build our portfolio of products.

TPF is well-provisioned for bad and doubtful debts – which are down year-

on-year and we also continue to see improving trends in credit card arrears.

Finance costs and tax Net finance costs were £63m (last year £126m),

reflecting favourable movements in the non-cash IFRS elements of the

interest charge. The interest charge, excluding IFRS adjustments and

finance income, rose 18%.

Total Group tax has been charged at an effective rate of 24.0% (last

year 29.1%). This reduction in tax rate is primarily due to a one-off tax

reimbursement, reflecting settlement of prior year tax items with HMRC.

We have also benefited from an adjustment of deferred tax balances as a

result of the lowering of the rate of UK corporation tax from 30% to 28%

with effect from 1 April 2008. We expect the effective tax rate for the

current year to be around 27.5%.

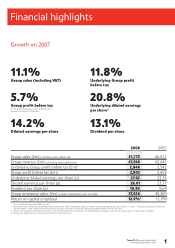

Underlying diluted earnings per share increased by 20.8% to 27.02p

(last year 22.36p), benefiting from the significantly lower than normal

effective tax rate for the year and from the elimination of earnings

dilution linked to new share issuance, resulting from our share buy-back

programme. On a normalised 28.9% tax rate basis, underlying diluted

earnings per share rose by 13.1%.

Dividend The Board has proposed a final dividend of 7.70p per share

(last year 6.83p). This represents an increase of 12.7%, and takes the full-

year increase in dividend to 13.1%. This increase in dividend is in line with

the growth in underlying diluted earnings per share, which are inclusive

of net property profits, using our normalised tax rate of 28.9%. Going

forward, we intend to continue to grow annual dividends broadly in line

with underlying diluted earnings per share growth.

The final dividend will be paid on 4 July 2008 to shareholders on

the Register of Members at the close of business on 25 April 2008.

Shareholders have the opportunity to elect to reinvest their cash

dividend and purchase existing Tesco shares in the Company through

a Dividend Reinvestment Plan. This scheme replaced the scrip dividend

at the time of the Interim Results in 2006 and was introduced to reduce

dilution from new share issuance and improve earnings per share.

Cash flow and Balance Sheet Group capital expenditure (excluding

acquisitions) rose to £3.9bn (last year £3.0bn); higher than the £3.5bn

forecast at our Interim Results. This increase was attributable to the

purchase of a small number of UK trading stores from a competitor,

investment in new mixed-use development schemes during the second

half and higher International capital expenditure.

UK capital expenditure was £2.5bn (last year £1.9bn), including £987m

on new stores, £457m on extensions and refits and approximately £200m

relating to our US operations, slightly below the guidance we gave last

November. Total International capital expenditure rose to £1.4bn (last year

£1.1bn) comprising £0.7bn in Asia and £0.7bn in Europe.

We expect Group capital expenditure to rise this year, driven largely by the

expansion of our International business, to around £4.2bn. This growth

will primarily arise from the increased scale of our investment in freehold

shopping centre developments in China. The change in the status of our

investment in China to a subsidiary, means that such developments will

now be fully funded directly from Tesco’s balance sheet.

Cash flow from operating activities, including an improvement of £194m

within working capital, totalled £4.1bn (last year £3.5bn). Net borrowings

rose to £6.2bn at the year end (last year £4.9bn). £0.6bn of this increase

is attributable to the effect of unfavourable currency movements on our

International balance sheet hedging (Sterling has depreciated by 11.5%

against the currencies of the countries in which we operate). A further

£0.3bn relates to acquisitions, including our share of Dobbies Garden

Centres PLC. Gearing was 52%.

Pensions Our award-winning defined-benefit pension scheme is an

important part of our competitive package of pay and benefits, which helps

Tesco recruit and retain the best people. We manage and fund our scheme

on an actuarial valuation basis and, as at December 2007, the scheme was

estimated to be broadly fully funded. As at February 2008, under the IAS 19

methodology of pension liability valuation, the Group pension deficit on a

post-tax basis was £603m.

Return on capital employed In January 2004, we said that we had

an aspiration to increase our post-tax return on capital employed (ROCE)

of 10.2% in the 2002/3 financial year by 200 basis points over five years

on then current plans. In April 2006, we renewed our commitment to

increasing our post-tax return on capital employed (ROCE) by a further

200 basis points, having exceeded our 2004 aspiration early.

ROCE rose to 12.9% in the year, using a normalised tax rate, before

start-up costs on the US and Tesco Direct and the impact of foreign

exchange equity and our acquisition of a majority share in Dobbies

(last year ROCE was 12.6%, excluding the Pensions A-Day credit).

This represents a good performance and we remain on track to deliver

our targeted ROCE improvement in the years ahead as these

investments mature.

www.tesco.com/annualreport08

Business Review continued