Walgreens 2006 Annual Report Download - page 24

Download and view the complete annual report

Please find page 24 of the 2006 Walgreens annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

-

36

-

37

-

38

|

|

The task force reached a conclusion that either method is acceptable, however, if

taxes are reported on a gross basis (included as sales) a company should disclose

those amounts if significant. Sales taxes are not included in revenues; however,

we are still evaluating the impact of this pronouncement on other taxes.

In July 2006, the FASB issued FIN 48, “Accounting for Uncertainty in Income Taxes

– an interpretation of FASB Statement No.109.” This interpretation clarifies the

accounting and disclosure for uncertain income tax positions, which relate

to the uncertainty about how certain income tax positions should be reflected

in the financial statements before they are resolved with the tax authorities.

This interpretation will be effective first quarter of fiscal 2008. We are currently

reviewing this pronouncement to determine the impact that it may have on our

consolidated financial position or results of operations.

In September 2006, the FASB issued SFAS No.157, “Fair Value Measurements.”

This statement defines and provides guidance when applying fair value measure-

ments to accounting pronouncements that require or permit such measurements.

This statement, which will be effective first quarter of fiscal 2009, is not expected

to have a material impact on our consolidated financial position or results

of operations.

In September 2006, the Securities and Exchange Commission (SEC) issued Staff

Accounting Bulletin (SAB) No.108. This SAB addresses diversity in practice in

quantifying financial statement misstatements. It also addresses the facts to

consider when evaluating the materiality of the error and the need to restate the

financial statements. This interpretation is effective for our first quarter of fiscal

2007 and will be followed if and when necessary.

In October 2006, the FASB issued SFAS No.158, “Employers’ Accounting for

Defined Benefit Pension and Other Postretirement Plans.” Companies will be

required to reflect the plan’s funded status on the balance sheet. The difference

between the plan’s funded status and its current balance sheet position would be

recognized, net of tax, as a component of Accumulated Other Comprehensive

Income. Had this statement been effective as of August 31, 2006, the impact to

Accumulated Other Comprehensive Income would have been $39.9 million. This

pronouncement will be effective for the company’s fourth quarter of fiscal 2007.

Cautionary Note Regarding Forward-Looking Statements

Certain statements and projections of future results made in this report constitute

forward-looking information that is based on current market, competitive and

regulatory expectations that involve risks and uncertainties. Please see Walgreen

Co.’s Form 10-K for the period ended August 31, 2006, for a discussion of

important factors as they relate to forward-looking statements. Actual results

could differ materially.

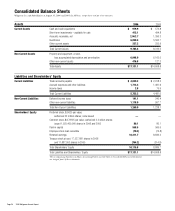

Off-Balance Sheet Arrangements

Letters of credit are issued to support purchase obligations and commitments

(as reflected on the Contractual Obligations and Commitments table) as follows

(In Millions):

Inventory obligations $105.1

Real estate development 1.7

Insurance 282.2

Total $389.0

We have no other off-balance sheet arrangements other than those disclosed

on the previous Contractual Obligations and Commitments table.

Both on-balance sheet and off-balance sheet financing are considered when

targeting debt to equity ratios to balance the interests of equity and debt

(real estate) investors. This balance allows us to lower our cost of capital while

maintaining a prudent level of financial risk.

Recent Accounting Pronouncements

In March 2005, the Financial Accounting Standards Board (FASB) issued

Interpretation (FIN) 47, “Accounting for Conditional Asset Retirement Obligations,”

which became effective in our fourth quarter fiscal 2006. This interpretation clarifies

that the term

conditional asset retirement obligation

as used in FASB SFAS No.143

refers to a legal obligation to perform an asset retirement activity in which the tim-

ing and/or method of settlement are conditional on a future event that may or may

not be within the control of the entity. We have adopted this interpretation and have

determined that there is no impact on our financial statements.

In May 2005, the FASB issued SFAS No.154, “Accounting Changes and Error

Corrections,” which will be effective in the first quarter of fiscal 2007. This statement

addresses the retrospective application of such changes and corrections and will

be followed if and when necessary.

In November 2005, the FASB issued Staff Position (FSP) 123(R)-3, “Transition

Election Related to Accounting for the Tax Effects of Share-Based Payment

Awards.” This pronouncement provides an alternative transition method

of calculating the excess tax benefits available to absorb any tax deficiencies

recognized subsequent to the adoption of SFAS No.123(R). The company has

elected to adopt the alternative transition method.

In June 2006, the FASB ratified Emerging Issues Task Force (EITF) Issue No.06-3,

“How Taxes Collected from Customers and Remitted to Governmental Authorities

Should Be Presented in the Income Statement (That Is, Gross versus Net

Presentation).” This pronouncement will be effective third quarter of fiscal 2007.

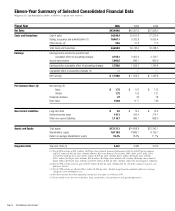

Management’s Discussion and Analysis of Results of Operations

and Financial Condition (continued)

Contractual Obligations and Commitments

The following table lists our contractual obligations and commitments at August 31, 2006 (In Millions):

Payments Due by Period

Less Than

Total 1 Year 1-3 Years 3-5 Years Over 5 Years

Operating leases

(1)

$26,086.3 $1,457.8 $3,020.8 $2,956.3 $18,651.4

Purchase obligations

(2)

:

Open inventory purchase orders 1,588.1 1,588.1 — — —

Real estate development 782.8 778.8 4.0 — —

Other corporate obligations 588.0 240.8 231.3 102.0 13.9

Insurance* 449.9 145.1 160.0 79.0 65.8

Retiree health & life* 294.0 7.8 18.5 23.0 244.7

Closed location obligations* 69.8 17.0 25.5 14.7 12.6

Capital lease obligations* 39.6 .9 2.1 2.4 34.2

Other long-term liabilities reflected on the balance sheet* 479.1 42.7 55.9 46.9 333.6

Total $30,377.6 $4,279.0 $3,518.1 $3,224.3 $19,356.2

* Recorded on balance sheet.

(1) Amounts for operating leases (nominal dollar) and capital leases do not include certain operating expenses under these leases such as common area

maintenance, insurance and real estate taxes. These expenses for the company’s most recent fiscal year were $228.8 million.

(2) Purchase obligations include agreements to purchase goods or services that are enforceable and legally binding and that specify all significant terms,

including open purchase orders.

Page 22 2006 Walgreens Annual Report