BP 2012 Annual Report Download - page 14

Download and view the complete annual report

Please find page 14 of the 2012 BP annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

|

|

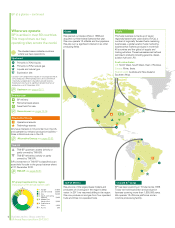

Energy outlook

Looking ahead, we expect demand for energy to grow

and the challenges facing our industry to be met by a diverse mix

of fuels and technologies.

Our market in 2012

World economic growth was weak in 2012 –

below its historic trend – and we expect

subdued global growth to continue in 2013.

Emerging economies with stronger productivity

and rising populations, led by China and India,

are set to drive growth. Developed countries

may lag as they continue to address internal

fiscal imbalances.

Global demand for energy, including oil,

continued to expand modestly in 2012, with

a weak economy and high oil prices weighing

on demand.

As a result, the growth in world oil consumption

remained weak in 2012, with continued growth

in China and other non-OECD countries

offsetting yet another decline in OECD

countries. With oil markets balancing lower

production from certain countries against weak

consumption and high OPEC production,

average crude oil prices in 2012 were similar to

the previous year, averaging $111.67 per barrel.

Natural gas prices continued to diverge globally

in 2012, with lower prices in the US and

increases in Europe and the Far East.

Crude prices

For more information on crude oil and

natural gas prices see page 64.

Globally, refining margins improved on average

as refinery closures and operational issues

reduced product supply. Demand continues to

grow in non-OECD countries but the weak

financial environment in OECD countries has

seen demand growth weaken.

Refining margins

For more information on the BP refining

marker margin and other measures see

page 73.

Concerns about the volatility of commodity

and financial markets, energy security and

climate change have led to continued debate

over the appropriate role of markets,

government regulation and other policy

measures that affect the supply and

consumption of energy. Given the pressures

in the sector, we expect regulation and taxation

of the energy industry and energy users to

increase in many areas in the future.

2010 2011 2012

150

125

100

75

50

25

2008 2009

Source: Platts/BP.

*See Downstream on page 73 for further information on RMM.

Dated Brent oil price

Average refining

marker margin (RMM)*

Henry Hub gas price

(First of Month Index)

Crude oil and gas prices, and refining

margins ($ per barrel of oil equivalent)

Business review: Group overview

BP Annual Report and Form 20-F 2012

12