BP 2012 Annual Report Download - page 15

Download and view the complete annual report

Please find page 15 of the 2012 BP annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

|

|

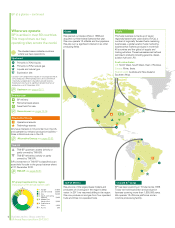

Longer-term outlook

Challenges and opportunities

The world’s population is projected to increase

by 1.3 billion from 2011 to 2030, with real

income likely to double over the same period.

These factors will lead to increased energy

demand and consumption. Energy and climate

policies, efficiency gains and a long-term

structural shift in fast-growing economies away

from industry and towards less energy-intensive

activities will help to restrain any increase, but

the overall trend is likely to be one of strong

growth. We expect demand for energy to

increase by as much as 36% between 2011 and

2030, with nearly 93% of the growth to occur in

non-OECD countries.

We estimate that there are enough energy

resources available to meet the increases in

demand in the foreseeable future, but there will

be challenges as well as opportunities.

Energy security represents a challenge. More

than 60% of the world’s natural gas is

concentrated in just four countries. More than

80% of global oil reserves are located in nine

countries, most of which are well away from the

hubs of energy consumption.

Meeting growing demand for secure and

sustainable energy will also present an

affordability challenge as the availability of easily

accessible fossil fuels slowly diminishes, with

many lower-carbon resources and technologies

remaining costly to produce at scale.

While energy is available to meet growing

demand, action is needed to limit carbon dioxide

(CO2) and other greenhouse gases being

emitted through fossil fuel use. Burning fossil

fuels can also raise local and regional air quality

issues.

Meeting the energy challenge

We believe that, increasingly, the global energy

challenge can only be met through a diverse mix

of fuels and technologies. A broad mix can

enhance national and global energy security

while supporting the transition to a lower-carbon

economy. This is one reason why BP’s portfolio

includes oil sands, shale gas, deepwater oil and

natural gas production, biofuels and wind.

We estimate that today’s oil reserves could

meet more than 45 years of demand at current

consumption rates, while known supplies of

natural gas could meet demand for nearly 60

years and coal could meet demand for up to

120 years.a

Our industry has a track record in expanding the

availability of resources through investment and

the application of technology. For example, in

1981 the world’s oil reserves stood at an

estimated 700 billion barrels. By 2011 this had

risen to 1,650 billion barrels, even though

800 billion barrels had been consumed in the

intervening three decades.

Oil and natural gas

We believe oil and natural gas are likely to

represent about 53% of total energy

consumption in 2030. Even under the

International Energy Agency’s (IEA) most

ambitious climate policy scenario (the 450

scenario), oil and gas would still make up 50%

of the energy mix in 2030, with combined

demand projected to exceed current levels in

absolute terms.b The 450 scenario assumes

governments adopt commitments to limit the

long-term concentration of greenhouse gases in

the atmosphere to 450 parts-per-million of CO2

equivalent.

The facts and figures used in this section are

derived from BP Energy Outlook 2030, published

in January 2013, unless otherwise indicated, and

represent a ‘base case’ or most likely projection.

1.6%per annum

Projected world primary energy

consumption growth to 2030.

a

BP Statistical Review of World Energy June 2012. These

reserve estimates are compiled from official sources and other

third-party data, which may not be based on proved reserves

as defined by SEC rules.

b From World Energy Outlook 2012©, OECD/IEA 2012, page 553.

2020

2030

18

16

14

12

10

8

6

4

2

1990 2000 2010

*Includes biofuels.

Source: BP Energy Outlook 2030.

Hydro Coal

Renewables* Nuclear

Oil

Gas

Energy consumption by fuel

(billion tonnes of oil equivalent)

Energy consumption by region

(billion tonnes of oil equivalent)

2020

2030

18

16

14

12

10

8

6

4

2

1990 2000 2010

Source: BP Energy Outlook 2030.

Non-OECD

OECD

In the US, our biofuels business is focusing on the

development of cellulosic ethanol technology at

facilities in San Diego, California (right) and

Jennings, Louisiana.

Business review: Group overview

BP Annual Report and Form 20-F 2012

13

Business review: Group overview

For more information see

bp.com/energyoutlook