HSBC 2007 Annual Report Download - page 15

Download and view the complete annual report

Please find page 15 of the 2007 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

|

|

13

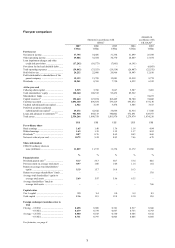

In calculating TSR, dividend income is assumed to

be invested in the underlying shares. As the

comparator group includes companies listed on

overseas markets, a common currency is used to

ensure that TSR is measured on a consistent basis.

The TSR benchmark is an index set at 100 and

measured over one, three and five years for the

purpose of comparison with the performance of a

group of competitor banks which reflect HSBC’s

range and breadth of activities. The TSR levels at the

end of 2007 were 95.6, 111.3, and 158.8 over one,

three and five years respectively. HSBC’s TSR over

all above mentioned periods has underperformed the

benchmark. This is attributed largely to the impact

on the share price of the current weakness in the US

sub-prime mortgage business and investor

preference over this time for companies with smaller

market values, particularly those for which there is

the possibility of participating in domestic or

regional consolidation.

Management believes that financial KPIs must

remain relevant to the business so they may be

changed over time to reflect changes in the Group’s

composition and the strategies employed.

Non-financial KPIs

HSBC has chosen four non-financial KPIs which are

important to the future success of the Group in

delivering its strategic objectives. These non-

financial KPIs are currently reported internally

within HSBC on a local basis.

Employee engagement

Employee engagement is a measure of employees’

emotional and rational attachment to HSBC.

In 2007, HSBC conducted its first Global

People Survey. This comprised questions designed to

measure employee engagement levels consistently

across the Group. The survey covers HSBC’s entire

permanent global workforce, and responses were

received from almost 290,000 employees, a response

rate of 88 per cent.

The overall employee engagement index score

was 60 per cent. The 2008 target is 62 per cent.

Survey questions were grouped into twelve

dimensions. Employees rated HSBC above the

external global norms in all these dimensions. In two

dimensions, reputation and corporate responsibility,

employees rated HSBC as achieving the external

best in class norm. The survey results have been

shared with all employees and action plans are being

developed at all levels of the organisation.

Brand perception

The score for brand perception is set by data

from surveys that are conducted by accredited,

independent, third party organisations. A weighted

score card is used to produce an overall score on a

100 point scale which is then benchmarked against

HSBC's main competitors. The scores from each

market are weighted according to the risk adjusted

revenues earned in that market to obtain the overall

company score.

The 2007 brand scores for Personal Financial

Services and Commercial Banking were ahead of the

competitor averages by 6 and 7 points, respectively,

on a 100 point scale. The 2008 brand perception

target is to increase the gap to 9 points and 8 points,

respectively.

Customer satisfaction

HSBC has regularly conducted customer satisfaction

surveys in its main markets over many years. HSBC

now uses a consistent measure of customer

recommendation to gauge customer satisfaction with

the services provided by the Group's Personal

Financial Services business. This survey is also

conducted by accredited, independent, third party

organisations and the resulting recommendation

scores are benchmarked against competitors.

The 2007 customer recommendation score for

Personal Financial Services was ahead of the

competitor average by 1 point on a 100 point scale.

The 2008 target is to increase that gap to 2.5 points.

IT performance and systems reliability

HSBC tracks two key measures as indicators of IT

performance; namely, the number of customer

transactions processed and the reliability and

resilience of systems measured in terms of service

availability targets.

Number of customer transactions processed

The number of customer transactions processed is a

reflection of the increasing usage of IT in each of the

delivery channels used to service customers. Its aim

is to manage the rate of increase in customer

transaction costs effectively and ensure that

customer growth is enabled in the appropriate

channels. The transition of customer transactions

from labour intensive (branch, call centre and others)

to automated (credit card, internet, self-service and

other e-channels) is occurring. The following chart

shows the 2005, 2006 and 2007 volumes per

delivery channel: