HSBC 2007 Annual Report Download - page 222

Download and view the complete annual report

Please find page 222 of the 2007 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

212 -

213

213 -

214

214 -

215

215 -

216

216 -

217

217 -

218

218 -

219

219 -

220

220 -

221

221 -

222

222 -

223

223 -

224

224 -

225

225 -

226

226 -

227

227 -

228

228 -

229

229 -

230

230 -

231

231 -

232

232 -

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

|

|

HSBC HOLDINGS PLC

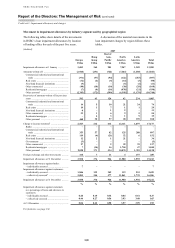

Report of the Directors: The Management of Risk (continued)

Credit risk > Areas of special interest > US personal lending / Loan delinquency in US

220

HSBC Finance: geographical concentration of US lending1

(Unaudited)

Mortgage lending as a

percentage of:

Other personal lending as a

percentage of

total

lending

total

mortgage

lending

total

lending

total other

personal

lending

Percentage

of total

lending

% % % % %

California ............................................................................... 6 12 6 12 12

Florida .................................................................................... 4 7 3 7 7

New York ............................................................................... 3 6 3 6 6

Texas ...................................................................................... 2 3 4 8 6

Ohio ....................................................................................... 3 5 2 5 5

Pennsylvania .......................................................................... 3 5 2 5 5

1 By states which individually account for 5 per cent or more of HSBC Finance’s US customer loan portfolio.

purchase of the property. For second lien

mortgages, the proportion of customers two months

or more behind on contractual payments rose from

3.97 per cent at 31 December 2006 to 9.02 per cent

at the end of 2007. Loss on default of second lien

loans approaches 100 per cent of the amount owed

as any collateral in the property is applied initially

to the first lien loan.

Stated-income mortgages are also of above

average risk as these were underwritten on the basis

of borrowers’ representations of annual income, not

verified by receipt of supporting documentation. In

HSBC Finance mortgage services, two months or

more delinquency rates on stated-income loans rose

from 6.36 per cent at 31 December 2006 to

19.01 per cent at 31 December 2007. In part, the

percentage rise is due to a decline in loan balances

as the mortgage loan portfolio is run off.

In mortgage services, the deterioration in credit

performance first reported in 2006 continued. In

the second half of 2007, credit quality became

progressively worse due to the market conditions

discussed above. Two months or more

delinquencies increased from US$2.3 billion,

4.64 per cent of loans and advances at the end

of 2006, to US$4.1 billion, 11.24 per cent at

31 December 2007. The increase in the

delinquency rate was partly due to the reduction

in the size of the portfolio.

In response, HSBC took several management

actions to reposition the US consumer business.

In March 2007, it took the decision to cease

purchasing mortgages from third party

correspondents. In September 2007, the Group

closed its wholesale business, Decision One,

ending new originations for the mortgage

services business.

The branch-based consumer lending business

experienced relatively stable performance in its

portfolio throughout 2006 and into the first half of

2007. Starting in the fourth quarter of 2006,

delinquencies began to rise in loans of 2005 and

later vintages, to levels above what had been

previously experienced. This trend was also seen in

the rest of the industry. It is clear that, for some

time, equity withdrawal has been the principal

source of credit available to sub-prime borrowers

dealing with unforeseen financial needs. Declining

house prices and an industry-wide tightening of

underwriting criteria have significantly reduced the

ability of consumers to refinance. Starting from the

third quarter, these factors had a marked effect on

consumer lending delinquency. Two months or

more delinquencies rose from 2.22 per cent at

31 December 2006 to 4.18 per cent of loans and

advances at the end of 2007. Delinquent balances

doubled to US$2.1 billion. In this environment,

HSBC took steps to tighten underwriting standards,

including decreasing the loan to value ratio for

residential mortgages and ceasing to underwrite

certain products. To match the consequent

reduction in demand and risk appetite, the network

was reduced from nearly 1,400 branches to some

1,000.

HSBC also sold parts of the loan portfolio

when opportunities arose at suitable valuations. In

the first half of 2007, a total of US$2.7 billion of

mortgage services’ loans that did not include any

loans 30 days or more delinquent were sold.

Credit card delinquencies of two months or

more rose from 4.48 per cent at the end of 2006 to

5.68 per cent of receivables at 31 December 2007.

In part, this was due to a change in product mix, as

originations in the sub-prime and near-prime parts

of the portfolio grew at faster rates than the overall

portfolio. There was also an increase in bankruptcy

rates as levels moved closer to historical norms

following the exceptionally low level of filings

seen during 2006. Additionally, in the fourth

quarter of 2007, delinquencies began to rise in all

vintages, particularly in the markets experiencing