NVIDIA 2006 Annual Report Download - page 56

Download and view the complete annual report

Please find page 56 of the 2006 NVIDIA annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

|

|

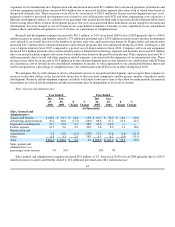

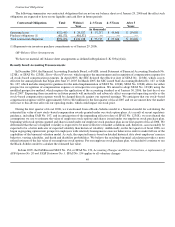

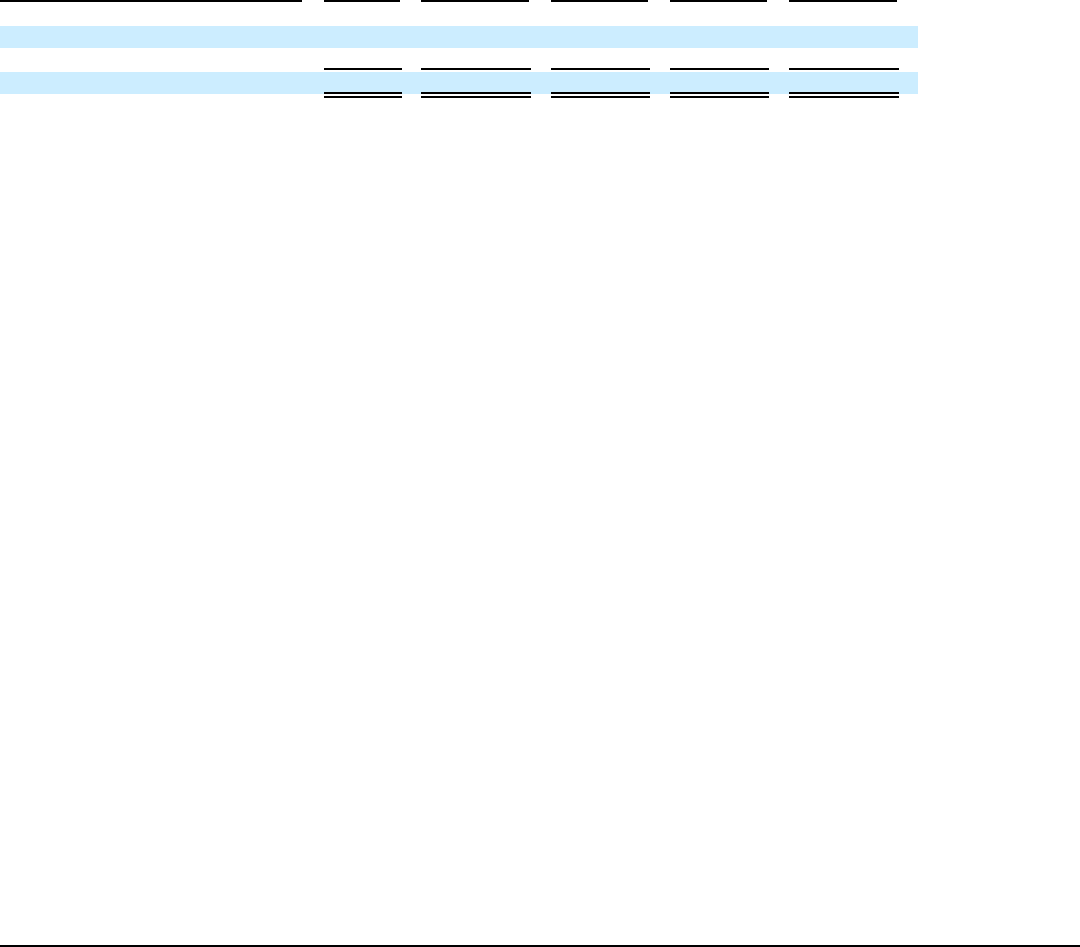

Contractual Obligations

The following summarizes our contractual obligations that are not on our balance sheet as of January 29, 2006 and the effect such

obligations are expected to have on our liquidity and cash flow in future periods:

Contractual Obligations Total Within 1

Year 2−3 Years 4−5 Years After 5

Years

(in thousands)

Operating leases $172,483 $ 29,557 $ 57,717 $ 55,606 $ 29,603

Purchase obligations (1) 401,571 401,571 −− −− −−

Total contractual obligations $574,054 $ 431,128 $ 57,717 $ 55,606 $ 29,603

(1) Represents our inventory purchase commitments as of January 29, 2006.

Off−Balance Sheet Arrangements

We have no material off−balance sheet arrangements as defined in Regulation S−K 303(a)(4)(ii).

Recently Issued Accounting Pronouncements

In December 2004, the Financial Accounting Standards Board, or FASB, issued Statement of Financial Accounting Standards No.

123(R), or SFAS No. 123(R), Share−Based Payment, which requires the measurement and recognition of compensation expense for

all stock−based compensation payments. In April 2005, the SEC delayed the effective date of SFAS No. 123(R), which is now

effective for annual periods that begin after June 15, 2005. In March 2005, the SEC issued Staff Accounting Bulletin No. 107, or SAB

No. 107, which includes interpretive guidance for the initial implementation of SFAS No. 123(R). SFAS No. 123(R) allows for either

prospective recognition of compensation expense or retrospective recognition. We intend to adopt SFAS No. 123(R) using the

modified prospective method, which requires the application of the accounting standard as of January 30, 2006, the first day of our

fiscal 2007. Expensing these incentives in future periods will materially and adversely affect our reported operating results as the

stock−based compensation expense would be charged directly against our reported earnings. We anticipate that our stock−based

compensation expense will be approximately $18 to $22 million for the first quarter of fiscal 2007 and we are unsure how the market

will react to this adverse affect on our operating results, which could impact our stock price.

During the first quarter of fiscal 2006, we transitioned from a Black−Scholes model to a binomial model for calculating the

estimated fair value of new stock−based compensation awards granted under our stock option plans. As a result of recent regulatory

guidance, including SAB No. 107, and in anticipation of the impending effective date of SFAS No. 123(R), we reevaluated the

assumptions we use to estimate the value of employee stock options and shares issued under our employee stock purchase plan,

beginning with stock options granted and shares issued under our employee stock purchase plan in our first quarter of fiscal 2006. We

determined that the use of implied volatility is expected to be more reflective of market conditions and, therefore, can reasonably be

expected to be a better indicator of expected volatility than historical volatility. Additionally, in the first quarter of fiscal 2006, we

began segregating options into groups for employees with relatively homogeneous exercise behavior in order to make full use of the

capabilities of the binomial valuation model. As such, the expected term is based on detailed historical data about employees' exercise

behavior, vesting schedules, and death and disability probabilities. We believe the resulting binomial calculation provides a more

refined estimate of the fair value of our employee stock options. For our employee stock purchase plan, we decided to continue to use

the Black−Scholes model to calculate the estimated fair value.

In June 2005, the FASB issued SFAS No. 154, or SFAS No. 154, Accounting Changes and Error Corrections, a replacement of

APB Opinion No. 20 and FASB Statement No. 3. SFAS No. 154 applies to all voluntary changes

49