Supercuts 2002 Annual Report Download - page 163

Download and view the complete annual report

Please find page 163 of the 2002 Supercuts annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

-

175

-

176

-

177

|

|

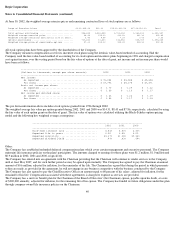

Generally, the goodwill recognized in the domestic transactions is expected to be fully deductible for tax purposes and the goodwill recognized

in the international transactions is non-deductible for tax purposes. The walk-in customer base of acquired salons was not recognized as an

identifiable intangible asset as the customers are not known or identifiable by the Company. Therefore, the value of the customer base is

recognized as part of residual goodwill. Internationally, the acquisition purchase price goodwill residual primarily represents the growth

prospects that are not captured as part of acquired tangible or identified intangible assets.

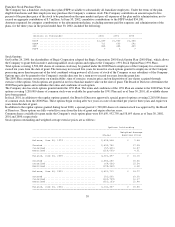

4. FINANCING ARRANGEMENTS:

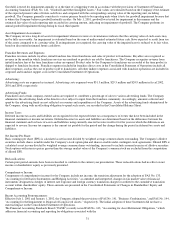

The Company's long-term debt as of June 30, 2002 and 2001 consists of the following:

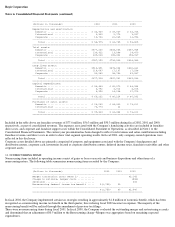

During March of fiscal 2002, the Company completed a $125.0 million private debt placement, with an average life of 8.6 years and a fixed

coupon rate of 6.98 percent. Proceeds were in part used to repay approximately $75.0 million of existing debt from the Company's revolving

credit facility. The additional $50.0 million of proceeds were primarily used to fund the Jean Louis David acquisition, which was completed in

April of 2002.

In October 2000, the Company borrowed $25 million under an 8.39 percent senior term note due October 2010 to finance various acquisitions

by the Company.

In September 2000, the Company amended its senior revolving credit agreement to increase the amount available from $180 million to $250

million, extending the expiration date to September 2003, and modifying certain debt covenant restrictions. The facility bears interest at the

prime rate or LIBOR plus 75 to 137.5 basis points based on the Company's debt-to-capitalization ratio and allows for multi-currency

borrowings. The prime rate at June 30, 2002 and 2001 was 4.75 percent and 6.75 percent, respectively. The revolving credit facility requires a

quarterly commitment fee of 15 to 25 basis points on the unused portion of the facility. The LIBOR credit spread and commitment fee are

based on the Company's debt-to-EBITDA ratio at the end of each fiscal quarter. The facility is used for short-term financing of new salon and

acquisition growth as well as to finance the general working capital requirements of the Company.

In June 2000, the Company extended the term of a $4.0 million note payment originally due July 1, 2000. The $4.0 million is the final payment

due under a $10.0 million senior term note entered into in October 1996. The maturity on the term note has been extended to September 2003.

The equipment and leasehold notes payable are primarily comprised of capital lease obligations totaling $4.0 million and $5.9 million at June

30, 2002 and 2001, respectively. These capital lease obligations are payable in monthly installments through 2005.

All of the Company's debt instruments are unsecured, except for its capital lease obligations which are collateralized by the assets purchased

under the agreement.

The debt agreements contain covenants, including limitations on incurrence of debt, granting of liens, investments, merger or consolidation,

and transactions with affiliates. In addition, the Company must not exceed specified fixed charge coverage, leverage and debt-to-capitalization

ratios.

As a result of the fair value hedging activities discussed in Note 5, an adjustment of approximately $2.3 million was made to increase the

carrying values of the Company's long-term fixed rate debt. Approximately 47 percent of the Company's fixed rate debt has been marked to

market. Considering the mark-to-market adjustment and current market interest rates, the carrying values of the Company's debt instruments,

based upon discounted cash flow analyses using the Company's current incremental borrowing rate, approximate their fair values at June 30,

2002.

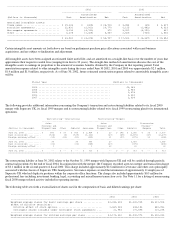

Aggregate maturities of long-term debt, including capital lease obligations at June 30, 2002, are as follows:

35

Interest Maturity

Rate % Dates 2002 2001

----------------------------------------------------------------------------------------------------

(Dollars in thousands)

Senior term notes ........................ 6.55- 8.39 2003-2012 $ 237,711 $ 113,163

Revolving credit facilities .............. 2.68- 8.23 2004 55,000 140,500

Equipment and leasehold notes payable .... 7.57-11.56 2004-2007 4,047 6,391

Other notes payable ...................... 5.00-10.00 2003-2009 2,258 1,504

------------------------

299,016 261,558

Less current portion ..................... (7,221) (5,438)

------------------------

Long-term portion ........................ $ 291,795 $ 256,120

========================

Fiscal Year (Dollars in thousands)

--------------------------------------------------------------------------------

2003..................................................... $ 7,221

2004..................................................... 76,863

2005..................................................... 15,750

2006..................................................... 12,549

2007..................................................... 22,037

Thereafter............................................... 164,596

--------------------------------------------------------------------------------

$299,016

================================================================================