TomTom 2007 Annual Report Download - page 73

Download and view the complete annual report

Please find page 73 of the 2007 TomTom annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

-

85

-

86

-

87

-

88

|

|

67

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

OF TOMTOM NV

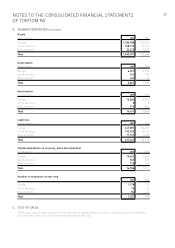

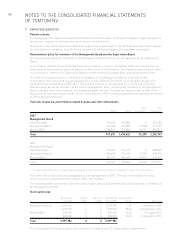

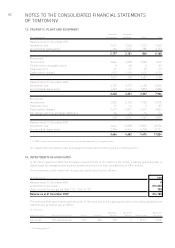

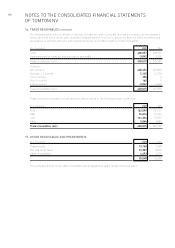

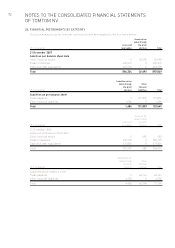

21. SHARE-BASED COMPENSATION (continued)

Performance share plan

The Group introduced a performance share plan to provide for employees, as the share option plans are being

phased out. Options are no longer being granted. Conditional awards of TomTom shares were made under the

share-based incentive plan of 2007. The actual amount of shares that may vest, ranging from 0-150% of the

conditional award, depends on the total shareholder return of TomTom compared to other companies listed in

the AEX index, and the EPS growth of TomTom. For the performance shares granted in 2007, the measurement

period is three years starting at 1 January 2007.

The following table provides more information about the performance shares which were conditionally awarded

in 2007:

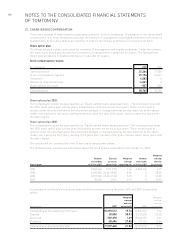

Share plan 2007

Outstanding at the beginning of the year 0

Granted 187,200

Exercised 0

Forfeited -2,100

Outstanding at the end of the year 185,100

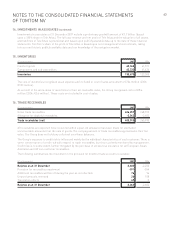

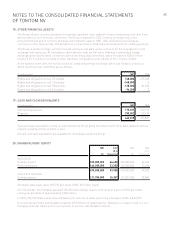

Valuation assumptions

The fair value of the share options granted up until March 2007 were determined by the Black and Scholes model.

The Black and Scholes model contains the input variables, including the risk-free interest rate, volatility of the

underlying share price, exercise price, and share price at the date of grant. The fair value calculated is allocated

on a straight-line basis over the three year vesting period, based on the Group’s estimate of equity instruments

that will eventually vest.

The fair value of the performance shares granted in 2007 was determined by the Black and Scholes model and

Monte Carlo pricing model. The models contain the input variables, including the risk-free interest rate, volatility

of the underlying share price, exercise price, and share price at the date of grant. The fair value is calculated

every reporting period based on the Group’s estimate of equity instruments that will eventually vest.

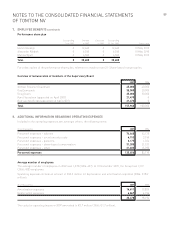

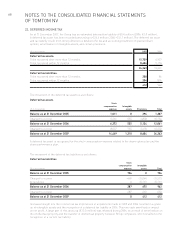

The input into the share option valuation model is as follows: 2007 2006

Weighted average share price (euro) 30.80 33.23

Weighted average exercise price (euro) 30.91 33.25

Weighted average expected volatility 40% 40%

Weighted average expected life 84 months 84 months

Weighted average risk free rate 3.96% 3.74%

Expected dividends Zero Zero

Volatility is determined using industry benchmarking for listed peer group companies, as well as the historic

volatility of the TomTom stock. The share price on the date of grant for options granted after the IPO is

determined as the three-day average of the stock price, prior to the date of the grant. Prior to the IPO, the share

price was determined by management, using a discounted cash flow model.

The Black and Scholes and the MonteCarlooption valuation models were developed for use in estimating the fair

value of traded options that have no vesting restrictions and are fully transferable. In addition, option valuation

models require the input of highly subjective assumptions, including the expected stock price volatility. The

Group’s employee stock options have characteristics significantly different from those of traded options, and

changes in the subjective input assumptions can materially affect the fair value estimate.