TomTom 2011 Annual Report Download - page 53

Download and view the complete annual report

Please find page 53 of the 2011 TomTom annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

|

|

51

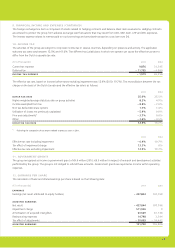

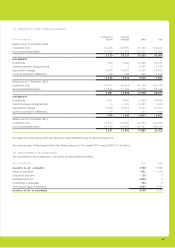

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONTINUED)

Trade receivables

Trade receivables are initially recognised at fair value, and subsequently measured at amortised cost (if the time value is material), using

the effective interest method, less provision for impairment. A provision for impairment of trade receivables is established when there is

objective evidence that the group will not be able to collect all amounts due, according to the original terms of the receivables.

The amount of the provision is the difference between the asset’s carrying amount and the present value of estimated future cash fl ows,

discounted at the original effective interest rate. The carrying amount of the asset is reduced through the use of an allowance account and

the amount of the loss is recognised in the income statement within ‘cost of sales’. When a trade receivable is uncollectible, it is written

off against the allowance account for trade receivables. Subsequent recoveries of amounts previously written off are credited against ‘cost

of sales’ in the income statement.

Cash and cash equivalents

Cash and cash equivalents are stated at face value and comprise cash on hand, deposits held on call with banks, and other short-term

highly liquid investments that are readily convertible to a known amount of cash and are subject to an insignifi cant risk of changes in value.

Financial liabilities and equity instruments

Financial liabilities and equity instruments issued by the group are classifi ed according to the substance of the contractual arrangements

entered into, and the defi nitions of a fi nancial liability and an equity instrument. An equity instrument is any contract that evidences a

residual interest in the assets of the group after deducting all of its liabilities. Equity instruments are recorded at the proceeds received,

net of direct issue costs.

Share capital

Ordinary shares are classifi ed as equity.

Share premium

The share premium represents the amount by which the fair value of the consideration received exceeds the nominal value of shares issued.

Incremental costs directly attributable to the issue of new shares or options are shown in equity as a deduction, net of tax, from

the proceeds.

Provisions

Provisions are recognised when the group has a present obligation as a result of a past event and it is probable that the group will be

required to settle that obligation. Provisions are measured at management’s best estimate of the expenditure required to settle the

obligation at the balance sheet date, and are discounted to present value where the effect is material.

Provisions for warranty costs are recognised at the date of sale of the relevant products, at management’s best estimate of the expenditure

required to settle the group’s obligation. Warranty costs are recorded within cost of sales.

Other provisions are recorded for probable liabilities that can be reasonably estimated. The provisions include legal claims, pension liabilities

and tax risks for which it is probable that an outfl ow of resources will be required to settle the obligation.

Borrowings

Borrowings are recognised initially at fair value, net of transaction costs incurred. Subsequently, amounts are stated at amortised cost with

the difference being recognised in the income statement over the period of the borrowings using the effective interest rate method.

3. FINANCIAL RISK MANAGEMENT

The business risks report included in this annual report contains auditable parts comprising ‘Credit’, ‘Liquidity’, ‘Loan covenants’, ‘Foreign

currencies’ and ‘Interest rates’. Management policies have been established to identify, analyse and monitor these risks, and to set

appropriate risk limits and controls. Financial risk management is carried out in accordance with the Treasury Policy, which has been

approved by the Supervisory Board. The written principles and policies are reviewed periodically to refl ect changes in market conditions

and the activities of the business.

Capital risk management

The group’s fi nancing policy aims to maintain a capital structure that enables the group to achieve its strategic objectives and daily

operational needs, and to safeguard the group’s ability to continue as a going concern.