Starbucks 2006 Annual Report Download - page 52

Download and view the complete annual report

Please find page 52 of the 2006 Starbucks annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

|

|

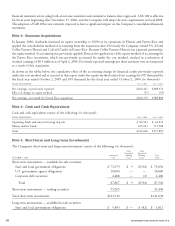

The following table shows the effect on net earnings and earnings per share had compensation cost been recognized based

upon the estimated fair value on the grant date of stock options, and ESPP, in accordance with SFAS 123, as amended by

SFAS No. 148 “Accounting for Stock-Based Compensation — Transition and Disclosure” (in thousands, except earnings

per share):

FISCAL YEAR ENDED Oct 2, 2005 Oct 3, 2004

Net earnings $494,370 $388,880

Deduct: stock-based compensation expense determined under fair value method, net of tax (58,742) (45,056)

Pro forma net income $435,628 $343,824

Earnings per share:

Basic — as reported $ 0.63 $ 0.49

Deduct: stock-based compensation expense determined under fair value method, net of tax (0.08) (0.06)

Basic — pro forma $ 0.55 $ 0.43

Diluted — as reported $ 0.61 $ 0.47

Deduct: stock-based compensation expense determined under fair value method, net of tax (0.08) (0.05)

Diluted — pro forma $ 0.53 $ 0.42

Disclosures for the year ended October 1, 2006 are not presented because the amounts are recognized in the consolidated

financial statements.

The fair value of stock awards was estimated at the date of grant using the Black-Scholes-Merton (“BSM”) option

valuation model with the following weighted average assumptions for the 52 weeks ended October 1, 2006, October 2,

2005 and 53 weeks ended October 3, 2004:

FISCAL YEAR ENDED 2006

2005

(Pro Forma)

2004

(Pro Forma) 2006

2005

(Pro Forma)

2004

(Pro Forma)

EMPLOYEE STOCK OPTIONS ESPP

Expected term (in years) 4.4 3.7 3.7 0.25 – 3.0 0.25 – 3.0 0.25 – 3.0

Expected stock price volatility 29% 33% 42% 22% – 50% 20% – 40% 19% – 43%

Risk-free interest rate 4.4% 3.5% 2.5% 2.3% – 5.0% 1.9% – 3.5% 0.9% – 2.3%

Expected dividend yield 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

Estimated fair value per option granted $9.59 $8.10 $5.30 $6.60 $5.05 $3.38

The expected term of the options represents the estimated period of time until exercise and is based on historical

experience of similar awards, giving consideration to the contractual terms, vesting schedules and expectations of future

employee behavior. For 2006, expected stock price volatility is based on a combination of historical volatility of the

Company’s stock and the one-year implied volatility of its traded options, for the related vesting periods. Prior to the

adoption of SFAS 123R, expected stock price volatility was estimated using only historical volatility. The risk-free interest

rate is based on the implied yield available on U.S. Treasury zero-coupon issues with an equivalent remaining term. The

Company has not paid dividends in the past and does not plan to pay any dividends in the near future.

The BSM option valuation model was developed for use in estimating the fair value of traded options, which have no

vesting restrictions and are fully transferable. In addition, option valuation models require the input of highly subjective

assumptions, particularly for the expected term and expected stock price volatility. The Company’s employee stock

options have characteristics significantly different from those of traded options, and changes in the subjective input

assumptions can materially affect the fair value estimate. Because Company stock options do not trade on a secondary

exchange, employees do not derive a benefit from holding stock options unless there is an increase, above the grant price,

in the market price of the Company’s stock. Such an increase in stock price would benefit all shareholders commen-

surately. See Note 14 for additional details.

48 STARBUCKS CORPORATION, FORM 10-K