Starbucks 2006 Annual Report Download - page 60

Download and view the complete annual report

Please find page 60 of the 2006 Starbucks annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

|

|

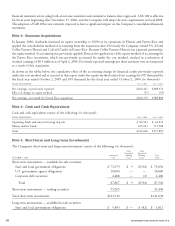

The following table summarizes goodwill by operating segment (in thousands):

FISCAL YEAR ENDED Oct 1, 2006 Oct 2, 2005

United States $125,976 $51,802

International 25,802 30,972

Global CPG 9,700 9,700

Total $161,478 $92,474

During fiscal 2006, the United States operating segment increased its equity ownership in its licensed operations in

Hawaii. During fiscal 2006, the International operating segment increased its equity ownership in its licensed operations

in Puerto Rico and made adjustments reducing goodwill upon the finalization of the purchase price of its Southern China

operations, for which it acquired majority ownership in the fiscal fourth quarter of 2005. The goodwill associated with

the Global CPG segment consists of portions allocated from the Company’s fiscal 1999 acquisition of Tazo Tea Company

and fiscal 2003 acquisition of Seattle Coffee Company, the parent company of Seattle’s Best Coffee LLC and Torrefazione

Italia LLC.

Note 10: Long-term Debt and Short-term Borrowings

In August 2005, the Company entered into a $500 million unsecured five-year revolving credit facility (the “facility”)

with various banks, of which $100 million may be used for issuances of letters of credit. The facility is available for

working capital, capital expenditures and other corporate purposes, which may include acquisitions and share repur-

chases. In August 2006, the Company increased its borrowing capacity under the facility to $1 billion, as provided in the

original credit facility. The interest rate for borrowings under the facility ranges from 0.150% to 0.275% over LIBOR or

an alternate base rate, which is the greater of the bank prime rate or the Federal Funds Rate plus 0.50%. The specific

spread over LIBOR will depend upon the Company’s performance under specified financial criteria.

As of October 1, 2006, the Company had $700 million outstanding, as well as a letter of credit of $11.9 million which

reduces the borrowing capacity under the credit facility. For the fiscal year ended October 1, 2006, the Company had

additional borrowings of $1.4 billion under the facility and made principal repayments of $993 million. As of October 2,

2005, the Company had $277 million outstanding, with no letters of credit. The weighted average contractual interest

rates at October 1, 2006 and October 2, 2005 were 5.5% and 4.0% respectively. The facility contains provisions that

require the Company to maintain compliance with certain covenants, including the maintenance of certain financial

ratios. As of October 1, 2006 and October 2, 2005, the Company was in compliance with each of these covenants.

In September 1999, Starbucks purchased the land and building comprising its York County, Pennsylvania roasting plant

and distribution facility for a total purchase price of $12.9 million. At the time of purchase, the Company assumed

related loans totaling $7.7 million from the York County Industrial Development Corporation. As of October 1, 2006,

the Company had $2.7 million outstanding. The remaining maturities of these loans range from four to five years, with

interest rates from 0.0% to 2.0%.

Interest expense, net of interest capitalized, was $8.4 million, $1.3 million and $0.4 million in fiscal 2006, 2005 and

2004, respectively. In fiscal 2006, $2.7 million of interest expense was capitalized for new store construction and included

in “Property, plant and equipment, net,” on the consolidated balance sheet. No interest was capitalized in fiscal 2005 or

2004.

56 STARBUCKS CORPORATION, FORM 10-K