Suzuki 2004 Annual Report Download - page 29

Download and view the complete annual report

Please find page 29 of the 2004 Suzuki annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

|

|

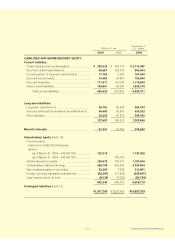

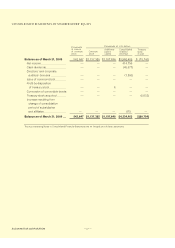

SUZUKI MOTOR CORPORATION

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

1. Basis of presenting consolidated financial statements

The accompanying consolidated financial statements of SUZUKI MOTOR CORPORATION (the

Company) have been prepared on the basis of generally accepted accounting principles and

practices in Japan, and the consolidated financial statements were filed with the Ministry of

Finance as required by the Securities and Exchange Law of Japan.

The preparation of the consolidated financial statements requires the management to select

and adopt accounting standards and make estimates and assumptions that affect the reported

amount of assets & liabilities and revenue & expenses and the corresponding methods of

disclosure.

As such, the management's estimates are made reasonably based on historical results etc. But

due to inherent uncertainty involving in making estimates, actual results could differ from these

estimates.

Certain reclassifications and modifications have been made to the original consolidated

financial statements for the convenience of readers outside Japan. In addition, the consolidated

statements of shareholders' equity have been prepared as additional information, although such

statements are not required in Japan, and the notes include information which is not required

under generally accepted accounting principles and practices in Japan.

As permitted, amount of less than one million yen have been omitted. For the convenience of

readers, the consolidated financial statements including the opening balance of shareholders'

equity have been presented in U.S. dollars by translating all Japanese yen amounts on the basis

of 105.69 to U.S.$1, the rate of exchange prevailing as of March 31, 2004. Consequently, the totals

shown in the consolidated financial statements (both in yen and in U.S. dollars) do not necessarily

agree with the sum of the individual amounts.

2. Summary of significant accounting policies

(a)Principles of consolidation

The consolidated financial statements for the years ended March 31, 2004 and 2003, include

the accounts of the Company and its significant subsidiaries and the number of consolidated

subsidiaries are 152 and 144 respectively. All significant inter-company accounts and

transactions are eliminated in consolidation. Investments in affiliated companies are accounted

for by the equity method.

As for the evaluation of assets and liabilities of consolidated subsidiaries, the complete market

value accounting method is adopted. The difference at the time of acquisition between the cost

and underlying net equity of investments in consolidated subsidiaries and in affiliated companies

accounted for under the equity method is, as a rule, amortized over a period of five years after

appropriate adjustments.

As for 50 companies of consolidated subsidiaries, their fiscal year end is December 31.

American Suzuki Motor Corp. and other 10 companies within above-mentioned 50 companies,

their accounts were consolidated based on their financial statements by the preliminary

settlement as of March 31, 2004.

The rest of 39 companies were consolidated based on their financial statements as of December

31, 2003. As a result of this change, the net sales increased by 15,952 million yen, the operating

income and net income increased by 832 million yen, 859 million yen, respectively.

(b)Allowance for doubtful receivables

The allowance for doubtful receivables is appropriated into the account for an estimated

uncollectible sum. If the financial condition of our customers deteriorates and their level of

solvency decreases, additional allowances or bad debt losses may be incurred.

29