Tesco 2004 Annual Report Download - page 6

Download and view the complete annual report

Please find page 6 of the 2004 Tesco annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

|

|

4TESCO PLC

OPERATING AND FINANCIAL REVIEW CONTINUED

JOINT VENTURES AND ASSOCIATES Our total share

of profit, before goodwill amortisation, from joint

ventures and associates was £99m compared to

£72m last year. Our share of Tesco Personal Finance

pre-tax profit, post minority interests has grown

significantly to £80m (2003 £48m).

FINANCIAL RISKS AND TREASURY MANAGEMENT The

treasury function is mandated by the Board to

manage the financial risks that arise in relation to

underlying business needs. The Board establishes

the functions policies and operating parameters

and routinely reviews its activities, which are also

subject to regular audit. The function does not

operate as a profit centre and the undertaking of

speculative transactions is not permitted.

The main financial risks faced by the Group relate

to the availability of funds to meet business needs,

the risk of default by counterparties to financial

transactions (credit risk), and fluctuations in interest

and foreign exchange rates. These risks are

managed as described below. The balance sheet

positions at 28 February 2004 are representative

of the positions throughout the year.

FUNDING AND LIQUIDITY The Group finances its

operations by a combination of retained profits,

long and medium-term debt capital market issues,

commercial paper, bank borrowings and leases. The

objective is to ensure continuity of funding. The

policy is to smooth the debt maturity profile, to

arrange funding ahead of requirements and to

maintain sufficient undrawn committed bank

facilities and a strong credit rating so that maturing

debt may be refinanced as it falls due.

The Groups long-term credit rating was confirmed

as stable during the year. Tesco Group is rated A1

by Moodys and A+ by Standard & Poors. New

funding of £621m was arranged during the year,

including a medium-term note of £98m maturing

in 2009 and crystallisation of interest swap profit

of £235m. A further £773m net proceeds was

raised through a share placing, which was used to

pay down debt. At the year end, net debt was

£4.1bn (2003 £4.7bn) and the average debt

maturity was nine years (2003 nine years).

Since the year end, we have conducted a property

deal with our joint venture partner Topland Group.

This provided £650m of competitive funding.

INTEREST RATE RISK MANAGEMENT The objective is

to limit our exposure to increases in interest rates.

Forward rate agreements, interest rate swaps, caps

and collars are used to achieve the desired mix

of fixed and floating rate debt. The policy is to fix

or cap a minimum of 40% of actual and projected

debt interest costs. Forward start interest rate

swaps are used to manage projected debt interest

costs where appropriate. At the year end £2.9bn,

71% of net debt, was in fixed rate form (2003

£2.6bn, 55%) with a further £135m, 3% of net

debt, collared as detailed in note 21. Fixed rate

debt includes £441m of funding linked to the Retail

Price Index (2003 £427m). This debt reduces

interest risk by diversifying our funding portfolio.

The balance of our debt is in floating rate form.

The average rate of interest paid during the year

was 5.6% (2003 5.7%). A 1% movement in UK

interest rates would change profit before tax by

less than 1%. Changes in interest rates in other

currencies would have no significant impact on

Group profits.

FOREIGN CURRENCY RISK MANAGEMENT Our principal

objective is to reduce the risk to short-term profits

of exchange rate volatility. Transactional currency

exposures that could significantly impact the profit

and loss account are hedged, typically using forward

purchases or sales of foreign currencies and

currency options. We hedge the balance sheet by

borrowing (either directly or via foreign exchange

transactions) in matching currencies where this is

cost effective. Our objectives are to maintain a

low cost of borrowing and retain some potential

for currency-related appreciation while partially

hedging against currency depreciation.

During the year, currency movements had minimal

impact on profits and decreased the net value of

the Groups assets by £157m (2003 £22m

increase). At the year end, forward foreign currency

purchases equivalent to £240m were outstanding

(2003 £240m). See note 21.

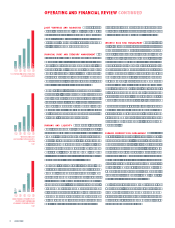

NUMBER OF INTERNATIONAL

HYPERMARKETS

152

152

102

102

68

68

38

38

00 01 02 03

194

04

INTERNATIONAL

UNDERLYING OPERATING

PROFIT

£m

212

212

119

119

74

74

50

50

00 01 02 03

306

04

TESCO PERSONAL FINANCE

PRE-TAX PROFIT/(LOSS)

POST MINORITY INTEREST

£m

9696

4040

6

(8)

00 01 02 03

160

04