US Postal Service 2006 Annual Report Download - page 56

Download and view the complete annual report

Please find page 56 of the 2006 US Postal Service annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

-

68

|

|

54 | 2006 Annual Report United States Postal Service

P.L.108-18

On April 23, 2003, the President signed into law P.L.108-18, the Postal

Civil Service Retirement System Funding Reform Act of 2003, which

changed the way we contribute to the CSRS retirement plan. Although

the law changed the funding of the plan, we determined that we would

still use multi-employer pension plan accounting treatment rules as an

“independent establishment of the executive branch of the United States

government.”

We are required by P.L.108-18 to pay an additional annual amount if

necessary, as determined by OPM, each September, beginning in 2004.

The “supplemental liability” represents the excess of the actuarial present

value of the future benefits liability over the actuarial present value of plan

assets, future contributions, earnings, and other actuarial factors related

to postal participants in the CSRS plan.

In September 2006, OPM estimated the present value of benefits at

$196.9 billion, contributions at $12.3 billion, and plan assets at $180.9

billion as of September 30, 2005. The calculated September 2005

“supplemental liability” of $3.7 billion, was a decrease of $500 million

from the $4.2 billion “supplemental liability” as of September 30, 2004.

This calculation assumed general salary increases of 2.8%, COLAs

of 3.25%, and interest of 6.25% and is intended to provide for the

liquidation of the “supplemental liability” over a 38-year period ending in

September 30, 2043. The following table presents OPM’s estimate of the

present value of our CSRS “Supplemental Liability.”

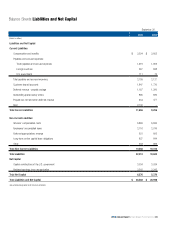

Present Value Analysis of CSRS

“Supplemental Liability” 2005 2004

(Dollars in billions as of September 30)

Present Value of Benefits $ 196.9 $ 195.0

Present Value of Contributions * $ 12.3 $ 14.1

Current Fund Balance $ 180.9 $ 176.7

Deficit $ (3.7) $ (4.2)

* Expected employer and employee contributions

Our “supplemental liability” payment in 2006 was $257 million, a

decrease of $33 million over the $290 million payment in 2005. Our first

“supplemental liability” payment in 2004 was $240 million.

P.L.108-18 also required that we place in escrow, by September 30,

2006, any “savings” until Congress decides the final disposition of

“savings” from the change in the retirement funding provisions. OPM

calculated the savings at $2,958 million.

Note 11 – Workers’ Compensation

We pay for workers’ compensation costs under a program administered

by DOL. These costs include employees’ medical expenses, payments for

continuation of wages and DOL administrative fees. We record these costs

as an operating expense.

Our liability at September 30, 2006, represents the estimated present

value of the total amount we expect to pay in the future for postal workers

injured through the end of 2006. The estimated total cost of a claim is

based upon the severity of the injury, the age of the injured employee, the

assumed life expectancy of the employee, the trend of our experience with

such an injury, and other factors.

In our calculation of present value for 2006 and 2005, a net discount rate

of -0.8% for medical expenses and 3.3% for compensation claims was

used. At the end of 2006, we estimate our total liability for future workers’

compensation costs at $7,863 million. At the end of 2005 this liability was

$7,521 million. The payout period for this liability will, for some claimants

currently on the rolls, be for the rest of their lives. The liability is sensitive

to changes in inflation and discount rates. An increase of 1% in the

assumptions would decrease our estimate of the liability by approximately

$676 million. A decrease of 1% would increase our estimate of the liability

by approximately $824 million.

In 2004, the net discount rates used to determine the present value

of estimated future workers’ compensation payments was changed, in

consultation with an independent actuary. Our net discount rate is the

estimated difference between what we expect to earn on investments

compared to what we assume the inflation rate will be for medical costs

and wage increases. Our net discount rate of -0.8% for medical claims

means that our assumptions show that the average rate of inflation for

medical claims of 5.5% will exceed our investment returns of 4.7% by

0.8% per year over the expected life of the medical claims. Conversely

we believe that our assumed investment returns of 5.5% will exceed the

rate of inflation on the consumer wages index of 2.2% by 3.3% over the

expected life of the compensation claims. Due to the differing average

lengths claimants stay on the rolls between medical and compensation

claims, we use two different market baskets of bonds funds to calculate

our expected returns.

In 2004, we reduced the medical claims net discount rate from 1.4% to

-0.8% resulting in an increase in our medical claims liability and expense

of $362 million. We increased the compensation claims net discount rate

from 3.0% to 3.3%, thereby reducing that liability and expense by $148

million. These combined changes increased our total workers’ compensa-

tion liability and expense by $214 million. The effect of the adoption of

these changes is accounted for as a change in accounting estimate as

defined by GAAP.

In 2006, we recorded $1,279 million in workers’ compensation expense,

compared to the $838 million in 2005 and $1,239 million recorded in

2004.

Notes to the Financial Statements

(3.7) (4.2)