ComEd 2003 Annual Report Download - page 90

Download and view the complete annual report

Please find page 90 of the 2003 ComEd annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

|

|

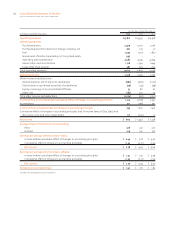

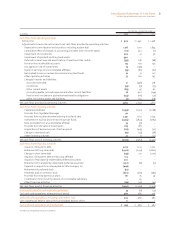

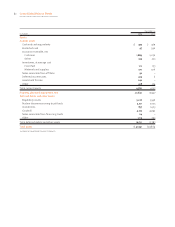

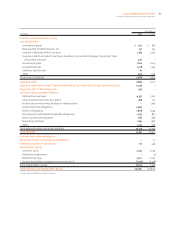

88 Notes to Consolidated Financial Statements

EXELON CORPORATION AND SUBSIDIARY COMPANIES

nuclear decommissioning trust funds for units acquired af-

ter the Merger are reported in other comprehensive income.

Prior to the adoption of SFAS No. 143, “Accounting for Asset

Retirement Obligations” (SFAS No. 143) on January 1, 2003,

unrealized gains and losses on marketable securities held in

the nuclear decommissioning trust funds were reported in

accumulated depreciation for operating units transferred to

Generation from PECO and as other comprehensive income

for operating and retired units transferred to Generation

from ComEd. At December 31, 2003 and 2002, Exelon had no

held-to-maturity securities.

Purchased Gas Adjustment Clause

PECO’s natural gas rates are subject to a fuel adjustment

clause designed to recover or refund the difference between

the actual cost of purchased gas and the amount included in

rates. Differences between the amounts billed to customers

and the actual costs recoverable are deferred and recovered

or refunded in future periods by means of prospective quar-

terly adjustments to rates. At December 31, 2003 and 2002,

deferred energy costs of $81 million and $31 million, re-

spectively, which are expected to be recovered under the

adjustment clause, were recorded in other current assets on

Exelon’s Consolidated Balance Sheets.

Property, Plant and Equipment

Property, plant and equipment is recorded at cost. The cost

of maintenance, repairs and minor replacements of property

is charged to maintenance expense as incurred.

Upon retirement, the cost of regulated property, net of

salvage, is charged to accumulated depreciation and re-

moval costs reduce the related regulatory liability in accord-

ance with the provisions of SFAS No. 71. See Note 6 – Property,

Plant and Equipment and Note 20 – Supplemental Financial

Information.

Nuclear Fuel

The cost of nuclear fuel is capitalized and charged to fuel

expense using the unit of production method. Estimated

costs of nuclear fuel storage and disposal, exclusive of dry

cask storage costs, at operating plants are charged to fuel

expense as the related fuel is consumed. Costs associated

with nuclear outages are recorded in the period incurred.

Dry cask storage costs are expensed as incurred.

Capitalized Software Costs

Costs incurred during the application development stage of

software projects that are developed or obtained for internal

use are capitalized. At December 31, 2003 and 2002, un-

amortized capitalized software costs totaled $630 million

and $491 million, respectively. Such capitalized amounts are

amortized ratably over the expected lives of the projects

when they become operational, not to exceed ten years. Cer-

tain capitalized software is being amortized over fifteen

years pursuant to regulatory approval. During 2003, 2002

and 2001, Exelon amortized capitalized software costs of $69

million, $64 million and $39 million, respectively.

Depreciation and Amortization

Depreciation is provided over the estimated service lives of

property, plant and equipment on a straight-line basis using

the composite method. Annual depreciation provisions for

financial reporting purposes, expressed as a percentage of

average service life for each asset category, are presented in

the table below. See Note 6 – Property, Plant and Equipment

for information on service life extensions for certain nuclear

generating stations and a change in Energy Delivery’s depre-

ciation rates.

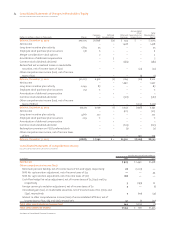

Asset Category 2003 2002 2001

Electric – transmission and distribution 2.81% 3.11% 3.97%

Electric – generation 2.90% 3.65% 3.11%

Gas 2.38% 2.13% 2.34%

Common – gas and electric 7.53% 6.40% 6.26%

Other property and equipment 8.20% 7.88% 9.53%

Amortization of regulatory assets is provided over the recov-

ery period specified in the related regulatory agreement.

Nuclear Generating Station Decommissioning

Exelon accounts for the costs of decommissioning its nuclear

generating stations in accordance with SFAS No. 143. See

Note 13 – Nuclear Decommissioning and Spent Fuel Storage

for information regarding the adoption and application of

SFAS No. 143 and Cumulative Effect of Changes in Accounting

Principle below for pro forma net income and earnings per

common share for the years ended December 31, 2002 and

2001, adjusted as if SFAS No. 143 had been applied effective

January 1, 2001.

Capitalized Interest and Allowance for Funds Used During

Construction

Exelon uses SFAS No. 34, “Capitalizing Interest Costs,” to cal-

culate the costs during construction of debt funds used to

finance its non-regulated construction projects. Exelon re-

corded capitalized interest of $15 million, $20 million and $17

million in 2003, 2002 and 2001, respectively.

Allowance for funds used during construction (AFUDC) is

the cost, during the period of construction, of debt and

equity funds used to finance construction projects for regu-

lated operations. AFUDC is recorded as a charge to con-

struction work in progress and as a non-cash credit to AFUDC

that is included in other income and deductions. The rates

used for capitalizing AFUDC are computed under a method

prescribed by regulatory authorities (see Note 20 – Supple-

mental Financial Information). Exelon recorded charges to

AFUDC of $16 million, $19 million and $19 million in 2003,

2002 and 2001, respectively.