McKesson 2015 Annual Report Download - page 109

Download and view the complete annual report

Please find page 109 of the 2015 McKesson annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

|

|

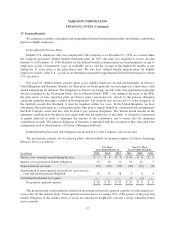

McKESSON CORPORATION

FINANCIAL NOTES (Continued)

Multiemployer Plans

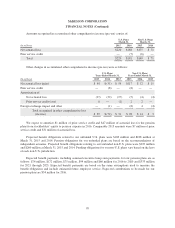

The Company contributes to a number of multiemployer pension plans under the terms of collective-

bargaining agreements that cover union-represented employees in the U.S. In 2015, we also contributed to the

Pensjonsordningen for Apoteketaten (“POA”), a mandatory multiemployer pension scheme for our pharmacy

employees in Norway, managed by the association of Norwegian Pharmacies.

The risks of participating in these multiemployer plans are different from single-employer pension plans in

the following aspects: (i) assets contributed to the multiemployer plan by one employer may be used to provide

benefits to employees of other participating employers; (ii) if a participating employer stops contributing to the

plan, the unfunded obligations of the plan may be borne by the remaining participating employers; and (iii) if the

Company chooses to stop participating in some of its multiemployer plans, the Company may be required to pay

those plans an amount based on the underfunded status of the plan, referred to as a withdrawal liability. Actions

taken by other participating employers may lead to adverse changes in the financial condition of a multiemployer

benefit plan and our withdrawal liability and contributions may increase.

Contributions and amounts accrued for U.S. Plans were not material for the years ended March 31, 2015,

2014, and 2013. Contributions to the POA for non-U.S. Plans exceeding 5% of total plan contributions were $24

million and $5 million in 2015 and 2014. Based on actuarial calculations, we estimate the funded status for our

non-U.S. Plans to be approximately 65% as of March 31, 2015. No amounts were accrued for liability associated

with the POA as we have no intention to withdraw from the plan.

Defined Contribution Plans

We have a contributory profit sharing investment plan (“PSIP”) for U.S. eligible employees. Eligible

employees may contribute to the PSIP up to 75% of their eligible compensation on a pre-tax or post-tax basis not

to exceed IRS limits. The Company makes matching contributions in an amount equal to 100% of the

employee’s first 3% of pay contributed and 50% for the next 2% of pay contributed. The Company also may

make an additional annual matching contribution for each plan year to enable participants to receive a full match

based on their annual contribution. The Company also contributed to non-U.S. plans that are available in certain

countries. Contribution expenses for the PSIP and non-U.S. plans were $103 million, $83 million and $65 million

for the years ended March 31, 2015, 2014, and 2013.

18. Postretirement Benefits

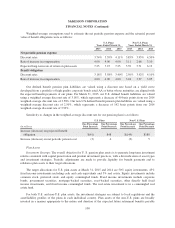

We maintain a number of postretirement benefits, primarily consisting of healthcare and life insurance

(“welfare”) benefits, for certain eligible U.S. employees. Eligible employees consist of those who retired before

March 31, 1999 and those who retired after March 31, 1999, but were an active employee as of that date, after

meeting other age-related criteria. We also provide postretirement benefits for certain U.S. executives. Defined

benefit plan obligations are measured as of the Company’s fiscal year-end.

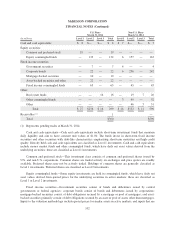

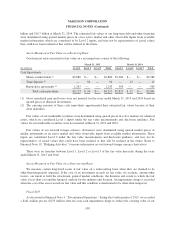

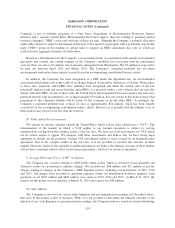

The net periodic expense for our postretirement welfare benefits is as follows:

Years Ended March 31,

(In millions) 2015 2014 2013

Service cost—benefits earned during the year $ 1 $ 2 $ 2

Interest cost on accumulated benefit obligation 5 5 6

Amortization of unrecognized actuarial gain and prior service credit (4) (1) (2)

Curtailment gain — (2) —

Net periodic postretirement expense $ 2 $ 4 $ 6

104