TCF Bank 2006 Annual Report Download - page 5

Download and view the complete annual report

Please find page 5 of the 2006 TCF Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

|

|

residential real estate. TCF’s secured lending strategy

reduces losses by providing a secondary source of repay-

ment in the event of a customer default. During 2006,

we saw the housing market soften and the Michigan

economy slow considerably. In the fourth quarter, TCF

experienced a moderate deterioration in credit quality,

especially in our Michigan consumer and commercial

loan portfolios. Overall, delinquencies remained at

acceptable levels, although they have increased from

prior periods.

3. Fee Income and Deposit Accounts

Although deposit service charges remained a challenging

area for TCF in 2006, progress was made. Fees and

service charges increased 2.9 percent in 2006 compared

to a 4.5 percent decline in 2005. Checking account

customers continued to change their banking behavior

by writing fewer checks, using their debit card more

frequently to replace check and cash transactions, and

doing more ACH transactions.

Deposit account growth was approximately 130,000

accounts, up 5.7 percent in 2006. We now have over

2.4 million deposit accounts. We also saw a decrease

in the frequency of NSF incidents in the second half

of 2006. It appeared this decrease was due to a more

conservative customer behavior, perhaps related to

uncertain economic conditions.

Debit card revenues continued their substantial growth

and increased 15.4 percent to $92.1 million in 2006.

TCF is currently the 13th largest Visa®Classic debit card

issuer in the United States. Debit card revenue growth

has slowed somewhat as this business is maturing and

our checking account growth has slowed over the past

few years.

Leasing revenues totaled $53 million, up 11.9 percent

from the prior year. Customer-driven sales-type lease

revenues declined while operating lease revenues

increased.

4. Power Assets®and Power Liabilities®

TCF’s Power Asset lending operations continued to

generate strong growth. Power Assets totaled $10.7

billion at the end of 2006 and increased 13.4 percent

over the prior year.

Consumer home equity loans grew 14.3 percent and

totaled $5.9 billion at year-end. Due to the flat or

inverted yield curve, the mix change from variable rate

2006 Annual Report 3

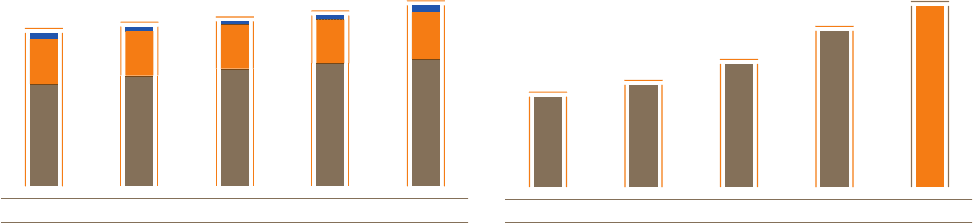

0605040302

2,427

2,296

2,216

2,150

2,067

Total Deposit Accounts

In Thousands

■ Checking

■ Savings & Money Market■ Certificates of Deposit

0605040302

$92.1

$79.8

$63.5

$53.0

$47.2

Card Revenue

Millions of Dollars