Wells Fargo 2012 Annual Report Download - page 164

Download and view the complete annual report

Please find page 164 of the 2012 Wells Fargo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

|

|

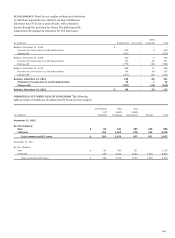

Note 6: Loans and Allowance for Credit Losses (continued)

The following table summarizes our TDR modifications for

the periods presented by primary modification type and includes

the financial effects of these modifications.

Primary modification type (1) Financial effects of modifications

Weighted Recorded

Other average investment

Interest interest interest related to

rate rate Charge- rate interest rate

(in millions) Principal (2) reduction concessions (3) Total offs (4) reduction reduction (5)

Year ended December 31, 2012

Commercial:

Commercial and industrial $ 11 35 1,370 1,416 40 1.60 % $ 38

Real estate mortgage 47 219 1,907 2,173 12 1.57 226

Real estate construction 12 19 531 562 10 1.69 19

Lease financing - - 4 4 - - -

Foreign - - 19 19 - - -

Total commercial 70 273 3,831 4,174 62 1.58 283

Consumer:

Real estate 1-4 family first mortgage 1,371 1,302 5,822 8,495 547 3.00 2,379

Real estate 1-4 family junior lien mortgage 79 244 756 1,079 512 3.70 313

Credit card - 241 - 241 - 10.85 241

Other revolving credit and installment 5 55 287 347 55 6.82 58

Trial modifications (6) - - 666 666 - - -

Total consumer 1,455 1,842 7,531 10,828 1,114 3.78 2,991

Total $ 1,525 2,115 11,362 15,002 1,176 3.59 % $ 3,274

Year ended December 31, 2011

Commercial:

Commercial and industrial $ 166 64 2,412 2,642 84 3.13 % $ 69

Real estate mortgage 113 146 1,894 2,153 24 1.46 160

Real estate construction 29 114 421 564 26 0.81 125

Lease financing - - 57 57 - - -

Foreign - - 22 22 - - -

Total commercial 308 324 4,806 5,438 134 1.55 354

Consumer:

Real estate 1-4 family first mortgage 1,629 1,908 934 4,471 293 3.27 3,322

Real estate 1-4 family junior lien mortgage 98 559 197 854 28 4.34 654

Credit card - 336 - 336 2 10.77 260

Other revolving credit and installment 74 119 7 200 24 6.36 181

Trial modifications (6) - - 651 651 - - -

Total consumer 1,801 2,922 1,789 6,512 347 4.00 4,417

Total $ 2,109 3,246 6,595 11,950 481 3.82 % $ 4,771

(1) Amounts represent the recorded investment in loans after recognizing the effects of the TDR, if any. TDRs with multiple types of concessions are presented only once in the

table in the first category type based on the order presented.

(2) Principal modifications include principal forgiveness at the time of the modification, contingent principal forgiveness granted over the life of the loan based on borrower

performance, and principal that has been legally separated and deferred to the end of the loan, with a zero percent contractual interest rate.

(3) Other interest rate concessions include loans modified to an interest rate that is not commensurate with the credit risk, even though the rate may have been increased.

These modifications would include renewals, term extensions and other interest adjustments, but exclude modifications that also forgive principal and/or reduce the interest

rate. Year ended December 31, 2012, includes $5.2 billion of consumer loans, consisting of $4.5 billion of first mortgages, $506 million of junior liens and $140 million of

auto and other loans, resulting from the OCC guidance issued in third quarter 2012, which requires consumer loans discharged in bankruptcy to be classified as TDRs, as well

as written down to net realizable collateral value.

(4) Charge-offs include write-downs of the investment in the loan in the period it is contractually modified. The amount of charge-off will differ from the modification terms if the

loan has been charged down prior to the modification based on our policies. In addition, there may be cases where we have a charge-off/down with no legal principal

modification. Modifications resulted in legally forgiving principal (actual, contingent or deferred) of $495 million and $577 million for years ended December 31, 2012 and

2011, respectively. Year ended December 31, 2012, includes $888 million in charge-offs on consumer loans resulting from the OCC guidance discussed above.

(5) Reflects the effect of reduced interest rates to loans with principal or interest rate reduction primary modification type.

(6) Trial modifications are granted a delay in payments due under the original terms during the trial payment period. However, these loans continue to advance through

delinquency status and accrue interest according to their original terms. Any subsequent permanent modification generally includes interest rate related concessions;

however, the exact concession type and resulting financial effect are usually not known until the loan is permanently modified. Trial modifications for the period are

presented net of any trial modifications that successfully complete the program requirements. Such successful modifications are included as an addition to the appropriate

loan category in the period they successfully complete the program requirements.

162