Apple 1998 Annual Report Download - page 18

Download and view the complete annual report

Please find page 18 of the 1998 Apple annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

|

|

proposed deficiencies by filing petitions with the United States Tax Court, and most of the issues in dispute have now been resolved. On June

30, 1997, the IRS proposed income tax adjustments for the years 1992 through 1994. Although a substantial number of issues for these years

have been resolved, certain issues still remain in dispute and are being contested by the Company. Management believes that adequate

provision has been made for any adjustments that may result from tax examinations.

The Company anticipates its effective tax rate for fiscal 1999 will be between 10% and 15%. The foregoing statements are forward looking.

The Company's actual results could differ because of several factors, including those set forth below in the subsection entitled "Factors That

May Affect Future Results and Financial Condition." Additionally, the actual future tax rate will be significantly impacted by the amount of

and jurisdiction in which the Company's foreign profits are earned.

LIQUIDITY AND CAPITAL RESOURCES

The following table presents selected financial information and statistics for each of the last three fiscal years (dollars in millions):

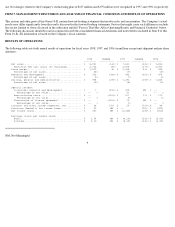

(a) Based on ending net trade receivables and most recent quarterly net sales for each period

(b) Based on ending inventory and most recent quarterly cost of sales for each period

As of September 25, 1998, the Company had $2.3 billion in cash, cash equivalents, and short-term investments, an increase of $841 million or

58% over the same balances at the end of fiscal 1997. During fiscal 1998, the Company's primary source of cash was $775 million in cash

flows from operating activities. Cash generated by operations was primarily from net income, declines in inventory and accounts receivable

resulting from improved asset management, and by a decline in other assets. These were partially offset by cash expenditures of $107 million

associated with the Company's restructuring program and a decrease in other current liabilities of $85 million. The Company's cash and cash

equivalent balances as of September 25, 1998, and September 26, 1997, include $56 million and $165 million, respectively, pledged as

collateral to support letters of credit.

In addition to the net purchase of short-term investments of $590 million, net cash used by investing activities included $46 million for the

purchase of property, plant, and equipment and $10 million paid for the acquisition of technology offset by proceeds of $89 million from the

sale of fixed assets and proceeds of $24 million from the sale of ARM stock. The Company expects that the level of capital expenditures in

1999 will be comparable to 1998.

Over the last three years, the Company's debt ratings have been downgraded to non-investment grade. As of March 27, 1998, the Company's

senior and subordinated long-term debt ratings were B- and CCC, respectively, by Standard and Poor's (S&P) Rating Agency, and B3 and

Caa2, respectively, by Moody's Investor Services (Moody's). In June 1998, Moody's upgraded the Company's senior debt to B2 from B3 and

subordinated debt to Caa1 from Caa2 citing strengthened debtholder protection measurements as the major reason for the upgrade. On

November 9, 1998, S&P upgraded the Company's senior debt to B+ from B

- and upgraded its subordinated debt to B- from CCC citing the

Company's improved profitability and financial profile for the upgrade. Despite these recent upgrades, the Company's continued non-

16

1998 1997 1996

--------- --------- ---------

Cash, cash equivalents, and short-term investments................................... $ 2,300 $ 1,459 $ 1,745

Accounts receivable, net............................................................. $ 955 $ 1,035 $ 1,496

Inventory............................................................................ $ 78 $ 437 $ 662

Working capital...................................................................... $ 2,178 $ 1,606 $ 2,512

Days sales in accounts receivable (a)................................................ 56 58 59

Days of supply in inventory (b)...................................................... 6 31 33

Operating cash flow.................................................................. $ 775 $ 154 $ 408