Charter 2008 Annual Report Download - page 27

Download and view the complete annual report

Please find page 27 of the 2008 Charter annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

|

|

Table of Contents

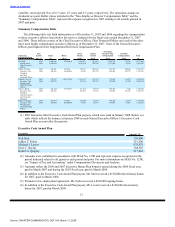

value for key executives. Pearl Meyer & Partners provided us with data regarding marketplace practices and

costs associated with retention programs. As a result of the 2006 Pearl Meyer & Partners compensation

analysis, the Compensation and Benefits Committee determined that the language and basic provisions of the

employment contracts for select executives should be made consistent to reflect some of the market terms

suggested by the Pearl Meyer & Partners’ analysis and recommendations including:

• Standardizing the employment agreement term at either two or three years, with automatic renewal

unless prior notice of non-renewal is provided;

• Standardizing the vesting of stock if the executive is not offered an equivalent position within six

months following any change-in-control; and

• Standardizing the severance formula to include base salary plus target bonus through the severance

period.

Also, as a result of the analysis and as furtherance of the retention of the select executives, the

Compensation and Benefits Committee provided for a special equity award that would be conditioned upon

the executive executing an employment agreement with the standard language as was acceptable to the

Company. The special equity award consisted of a mixture of performance units tied to 2007 performance and

restricted shares. The conversion of 2007 performance units to performance shares is discussed in

“Long-Term Incentive Program,” above.

Other Compensation Elements

The Named Executive Officers participate in all other benefit programs offered to all employees

generally.

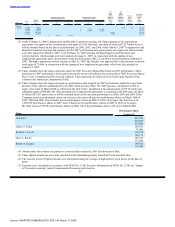

Impact of Tax and Accounting

Section 162(m) of the Internal Revenue Code generally provides that certain kinds of compensation in

excess of $1 million in any single year paid to the chief executive officer and the three other most highly

compensated executive officers other than the chief financial officer of a public company are not deductible

for federal income tax purposes. However, pursuant to regulations issued by the U.S. Treasury Department,

certain limited exemptions to Section 162(m) apply with respect to qualified “performance-based

compensation.” While the tax effect of any compensation arrangement is one factor to be considered, such

effect is evaluated in light of our overall compensation philosophy. To maintain flexibility in compensating

executive officers in a manner designed to promote varying corporate goals, the Compensation and Benefits

Committee has not adopted a policy that all compensation must be deductible. Stock options and performance

shares granted under our 2001 Stock Incentive Plan are subject to the approval of the Compensation and

Benefits Committee. The grants qualify as “performance-based compensation” and, as such, are exempt from

the limitation on deductions. Outright grants of restricted stock and certain cash payments (such as base salary

and cash bonuses) are not structured to qualify as “performance-based compensation” and are, therefore,

subject to the Section 162(m) limitation on deductions and will count against the $1 million cap.

When determining amounts and forms of compensation grants to executives and employees, the

Compensation and Benefits Committee considers the accounting cost associated with the grants. On

January 1, 2006, the Company adopted Statement of Financial Accounting Standard 123 (revised 2004),

Share — Based Payment (“SFAS No. 123R”), which addresses the accounting for share-based payment

transactions in which a company receives employee services in exchange for (a) equity instruments of that

company or (b) liabilities that are based on the fair value of the company’s equity instruments or that may be

settled by the issuance of such equity instruments. Under SFAS No. 123R, grants of stock options, restricted

stock, performance shares and other share-based payments result in an accounting charge for our company.

The accounting charge is equal to the fair value of the instruments being issued and is amortized over the

requisite service period, or vesting period of the instruments. For restricted stock and performance shares, the

cost is equal to the fair value of the stock on the date of grant times the number of shares or units granted. For

stock options, the cost is equal to the fair value of the option, estimated using the Black-Scholes

option-pricing model, times the number of options granted. The following weighted average assumptions

were used for grants during the years ended December 31, 2007, 2006 and 2005, respectively: risk-free

interest rates of 4.6%, 4.6% and 4.0%; expected volatility of 70.3%, 87.3%, and 70.9% based on historical

20

Source: CHARTER COMMUNICATIO, DEF 14A, March 17, 2008