Cisco 2010 Annual Report Download - page 32

Download and view the complete annual report

Please find page 32 of the 2010 Cisco annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

|

|

Management’s Discussion and Analysis of Financial Condition and Results of Operations

Fiscal 2009 Compared with Fiscal 2008

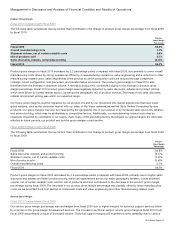

The provision for income taxes resulted in an effective tax rate of 20.3% for fiscal 2009, compared with 21.5% for fiscal 2008. The

net 1.2 percentage point decrease in the effective tax rates between fiscal years was attributable in part to a greater proportion of

net income which was subject to foreign income tax rates that are lower than the U.S. federal statutory rate of 35%. Additionally,

the effective tax rate of 20.3% for fiscal 2009 included a tax benefit of $106 million, or 1.4 percentage points, related to fiscal 2008

R&D expenses due to the retroactive reinstatement of the U.S. federal R&D tax credit offset by tax costs of $174 million, or 2.3

percentage points, related to a transfer pricing adjustment for share-based compensation. The transfer pricing adjustment was a

result of a decision by the Ninth Circuit to overturn a 2005 U.S. Tax Court ruling in a case to which we were not a party. The Ninth

Circuit decision impacted the tax treatment of share-based compensation expenses for the purpose of determining intangible

development costs under a company’s R&D cost sharing arrangement. The effective tax rate of 21.5% for fiscal 2008 included a net

tax benefit of $162 million, or 1.6 percentage points, from the settlement of certain tax matters with the IRS offset by tax costs of

$229 million, or 2.2 percentage points, related to the intercompany realignment of certain of our foreign entities.

Recent Accounting Standards or Updates

In June 2009, the FASB issued revised guidance for the consolidation of variable interest entities. In February 2010, the FASB

issued amendments to the consolidation requirements, exempting certain investment funds from the June 2009 guidance for the

consolidation of variable interest entities. The June 2009 guidance for the consolidation of variable interest entities replaces the

quantitative-based risks and rewards approach with a qualitative approach that focuses on identifying which enterprise has the

power to direct the activities of a variable interest entity that most significantly impact the entity’s economic performance and has

the obligation to absorb losses or the right to receive benefits from the entity that could be potentially significant to the variable

interest entity. The accounting guidance also requires an ongoing reassessment of whether an enterprise is the primary beneficiary

and requires additional disclosures about an enterprise’s involvement in variable interest entities. This accounting guidance is

effective for us beginning in the first quarter of fiscal 2011. Upon adoption, the application of the revised guidance for the

consolidation of variable interest entities did not have a material impact to our Consolidated Financial Statements.

In June 2009, the FASB issued revised guidance for the accounting of transfers of financial assets. This guidance eliminates the

concept of a qualifying special-purpose entity, removes the scope exception for qualifying special-purpose entities when applying

the accounting guidance related to the consolidation of variable interest entities, changes the requirements for derecognizing

financial assets, and requires enhanced disclosure. This accounting guidance is effective for us beginning in the first quarter of

fiscal 2011. Upon adoption, the application of the revised guidance for the accounting of transfers of financial assets did not have a

material impact to our Consolidated Financial Statements.

30 Cisco Systems, Inc.