Cisco 2010 Annual Report Download - page 35

Download and view the complete annual report

Please find page 35 of the 2010 Cisco annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

|

|

Management’s Discussion and Analysis of Financial Condition and Results of Operations

Financing Receivables We provide financing to certain end-user customers and channel partners to enable sales of our products,

services, and networking solutions. These financing arrangements include leases, financed service contracts, and loans. Arrangements

related to leases and loans are generally collateralized by a security interest in the underlying assets. Lease receivables include sales-

type and direct-financing leases. We also provide certain qualified customers financing for long-term service contracts, which primarily

relate to technical support services. Our loan financing arrangements may include not only financing the acquisition of our products and

services but also providing additional funds for other costs associated with network installation and integration of our products and

services. We expect to continue to expand the use of our financing programs in the near term.

Financing Guarantees In the normal course of business, third parties may provide financing arrangements to our customers and

channel partners under financing programs. The financing arrangements to customers provided by third parties are related to

leases and loans and typically have terms of up to three years. In some cases, we provide guarantees to third parties for these

lease and loan arrangements. The financing arrangements to channel partners consist of revolving short-term financing provided by

third parties, generally with payment terms ranging from 60 to 90 days. In certain instances, these financing arrangements result in

a transfer of our receivables to the third party. The receivables are derecognized upon transfer, as these transfers qualify as true

sales, and we receive payments for the receivables from the third party based on our standard payment terms. These financing

arrangements facilitate the working capital requirements of the channel partners and, in some cases, we guarantee a portion of

these arrangements. We could be called upon to make payments under these guarantees in the event of nonpayment by the

channel partners or end-user customers. Historically, our payments under such arrangements have been immaterial. Where we

provide a guarantee, we defer the revenue associated with the channel partner and end-user financing arrangement in accordance

with revenue recognition policies, or we record a liability for the fair value of the guarantees. In either case, the deferred revenue is

recognized as revenue when the guarantee is removed.

Deferred Revenue Related to Financing Receivables and Guarantees The majority of the deferred revenue in the preceding table is

related to financed service contracts. The revenue related to financed service contracts, which primarily relates to technical support

services, is deferred and included in deferred service revenue. The revenue related to financed service contracts is recognized

ratably over the period during which the related services are to be performed. A portion of the revenue related to lease and loan

receivables is also deferred and included in deferred product revenue based on revenue recognition criteria.

Borrowings

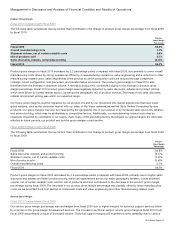

Senior Notes The following table summarizes the principal amount of our senior notes (in millions):

July 31, 2010 July 25, 2009

Increase

(Decrease)

Senior notes:

5.25% fixed-rate notes, due 2011 (“2011 Notes”) $ 3,000 $ 3,000 $ —

2.90% fixed-rate notes, due 2014 (“2014 Notes”) 500 — 500

5.50% fixed-rate notes, due 2016 (“2016 Notes”) 3,000 3,000 —

4.95% fixed-rate notes, due 2019 (“2019 Notes”) 2,000 2,000 —

4.45% fixed-rate notes, due 2020 (“2020 Notes”) 2,500 — 2,500

5.90% fixed-rate notes, due 2039 (“2039 Notes”) 2,000 2,000 —

5.50% fixed-rate notes, due 2040 (“2040 Notes”) 2,000 — 2,000

Total $ 15,000 $ 10,000 $ 5,000

In November 2009, we issued senior unsecured notes in an aggregate principal amount of $5.0 billion. Of these notes, $500 million

will mature in 2014 and bear interest at a fixed rate of 2.90% per annum (the “2014 Notes”), $2.5 billion will mature in 2020 and

bear interest at a fixed rate of 4.45% per annum (the “2020 Notes”), and $2.0 billion will mature in 2040 and bear interest at a fixed

rate of 5.50% per annum (the “2040 Notes”), as reflected in the preceding table. To achieve our interest rate risk management

objectives we entered into $1.5 billion notional amount interest rate swaps designated as fair value hedges of a portion of the 2016

Notes.

Interest is payable semi-annually on each class of the senior fixed-rate notes, each of which is redeemable by us at any time,

subject to a make-whole premium. We were in compliance with all debt covenants as of July 31, 2010.

Other Notes and Borrowings Other notes and borrowings include notes and credit facilities with a number of financial institutions

that are available to certain of our foreign subsidiaries. The amount of borrowings outstanding under these arrangements was $59

million and $2 million as of July 31, 2010 and July 25, 2009, respectively.

Credit Facility We have a credit agreement with certain institutional lenders that provides for a $3.0 billion unsecured revolving

credit facility that is scheduled to expire on August 17, 2012. Any advances under the credit agreement will accrue interest at rates

that are equal to, based on certain conditions, either (i) the higher of the Federal Funds rate plus 0.50% or Bank of America’s “prime

2010 Annual Report 33