DTE Energy 2007 Annual Report Download - page 15

Download and view the complete annual report

Please find page 15 of the 2007 DTE Energy annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

-

27

-

28

-

29

-

30

|

|

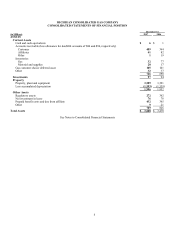

Business Combinations

In December 2007, the FASB issued SFAS No. 141(R), Business Combinations. The objective of this Statement is to improve the

relevance, representational faithfulness, and comparability of the information that a reporting entity provides in its financial reports

about a business combination and its effects. To accomplish that, this Statement establishes principles and requirements for how the

acquirer:

• Recognizes and measures in its financial statements the identifiable assets acquired, the liabilities assumed, and any

noncontrolling interest in the acquiree;

• Recognizes and measures the goodwill acquired in the business combination or a gain from a bargain purchase; and

• Determines what information to disclose to enable users of the financial statements to evaluate the nature and financial effects

of the business combination.

SFAS No. 141(R) shall be applied prospectively to business combinations for which the acquisition date is on or after the beginning of

the first annual reporting period beginning on or after December 15, 2008. Earlier adoption is prohibited. The Company is currently

assessing the effects of this statement, and has not yet determined its impact on its consolidated financial statements.

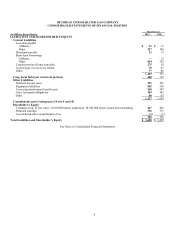

Noncontrolling Interests in Consolidated Financial Statements

In December 2007, the FASB issued SFAS No. 160, Noncontrolling Interests in Consolidated Financial Statements – an Amendment

of ARB No. 51. The standard requires:

• The ownership interests in subsidiaries held by parties other than the parent be clearly identified, labeled, and presented in the

consolidated statement of financial position within equity, but separate from the parent’ s equity;

• The amount of consolidated net income attributable to the parent and to the noncontrolling interest be clearly identified and

presented on the face of the consolidated statement of income;

• Changes in a parent’ s ownership interest while the parent retains its controlling financial interest in its subsidiary be accounted

for as equity transactions;

• When a subsidiary is deconsolidated, any retained noncontrolling equity investment in the former subsidiary be initially

measured at fair value. The gain or loss on the deconsolidation of the subsidiary is measured using the fair value of any

noncontrolling equity investment rather than the carrying amount of that retained investment; and

• Entities provide sufficient disclosures that clearly identify and distinguish between the interests of the parent and the interests

of the noncontrolling owners.

SFAS No. 160 is effective for fiscal years, and interim periods within those fiscal years, beginning on or after December 15, 2008.

Earlier adoption is prohibited. This Statement shall be applied prospectively as of the beginning of the fiscal year in which this

Statement is initially applied, except for the presentation and disclosure requirements. The presentation and disclosure requirements

shall be applied retrospectively for all periods presented. The Company is currently assessing the effects of this statement, and has not

yet determined its impact on its consolidated financial statements.

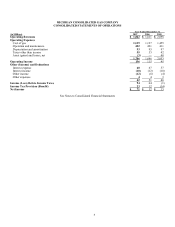

Stock-Based Compensation

Effective January 1, 2006, our parent company, DTE Energy, adopted SFAS No. 123(R), Share-Based Payment, using the modified

prospective transition method. We receive an allocation of costs associated with stock compensation and the related impact of

cumulative accounting adjustments. Our allocations for 2007 and 2006 for stock-based compensation expense were approximately $3

million and $2 million, respectively. The cumulative effect of the adoption of SFAS 123(R) had an immaterial impact on our operation

and maintenance expense. We have not restated any prior periods as a result of the adoption of SFAS 123(R).

13