DTE Energy 2007 Annual Report Download - page 16

Download and view the complete annual report

Please find page 16 of the 2007 DTE Energy annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

-

28

-

29

-

30

|

|

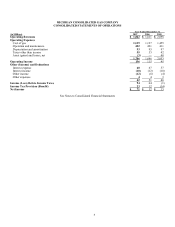

NOTE 3 – RESTRUCTURING

Performance Excellence Process

In mid-2005, we initiated a company-wide review of our operations called the Performance Excellence Process. We began a series of

focused improvement initiatives and expect this process will continue into 2008.

We have incurred costs to achieve (CTA) for employee severance and other costs, consisting primarily of project management and

consultant support. We cannot defer CTA costs at this time because a recovery mechanism has not been established. We expect to

seek a recovery mechanism in our next rate case in 2009.

Amounts expensed are recorded in the Operation and maintenance line on the Consolidated Statements of Operations. Costs incurred

in 2007 and 2006 are as follows:

Employee Severance Costs Other Costs Total Cost

(in Millions) 2007 2006 2007 2006 2007 2006

Costs incurred $ 3 $ 17 $ 6 $ 7 $ 9 $ 24

A liability for future CTA associated with the Performance Excellence Process has not been recognized because the Company has not

met the recognition criteria of SFAS No. 146, Accounting for Costs Associated with Exit or Disposal Activities.

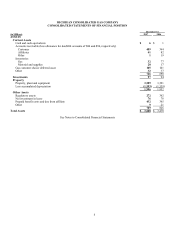

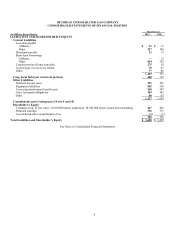

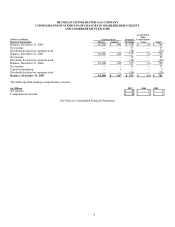

NOTE 4 – REGULATORY MATTERS

Regulation

We are subject to the regulatory jurisdiction of the MPSC, which issues orders pertaining to rates, recovery of certain costs, including

the costs of regulatory assets, conditions of service, accounting and operating-related matters.

Regulatory Assets and Liabilities

We apply the provisions of SFAS No. 71, Accounting for the Effects of Certain Types of Regulation. SFAS No. 71 requires the

recording of regulatory assets and liabilities for certain transactions that would have been treated as revenue and expense in non-

regulated businesses. Continued applicability of SFAS No. 71 requires that rates be designed to recover specific costs of providing

regulated services and be charged to and collected from customers. Future regulatory changes or changes in the competitive

environment could result in the Company discontinuing the application of SFAS No. 71 for some or all of its business and require the

write-off of the portion of any regulatory asset or liability that was no longer probable of recovery through regulated rates.

Management believes that currently available facts support the continued application of SFAS No. 71.

The following are the balances of the regulatory assets and liabilities as of December 31:

(in Millions) 2007 2006

Assets

Deferred environmental costs $ 39 $ 38

Unamortized loss on reacquired debt 29 30

Recoverable pension and postretirement costs 116 260

Recoverable uncollectibles expense 66 45

Deferred income taxes – Michigan Business Tax 47 —

297 373

Less amount included in current assets (25) (11)

$ 272 $ 362

Liabilities

Asset removal costs $ 363 $ 354

Refundable income taxes 104 114

Accrued GCR refund 70 81

Safety and training cost refund — 3

Accrued pension 71 39

Deferred income taxes – Michigan Business Tax 47 —

655 591

Less amount included in current liabilities and other liabilities (70) (81)

$ 585 $ 510

14