DTE Energy 2007 Annual Report Download - page 17

Download and view the complete annual report

Please find page 17 of the 2007 DTE Energy annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

-

29

-

30

|

|

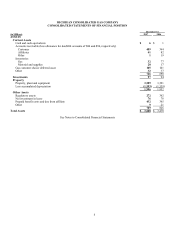

ASSETS

• Deferred environmental costs — The MPSC approved the deferral and recovery of investigation and remediation costs

associated with former MGP sites.

• Unamortized loss on reacquired debt — The unamortized discount, premium and expense related to debt redeemed with a

refinancing are deferred, amortized and recovered over the life of the replacement issue.

• Recoverable pension and postretirement costs — The traditional rate setting process allows for the recovery of pension and

postretirement costs as measured by generally accepted accounting principles.

• Recoverable uncollectibles expense — Receivable for the MPSC approved uncollectible expense true-up mechanism that

tracks the difference in the fluctuation in uncollectible accounts and amounts recognized pursuant to the MPSC authorization.

• Deferred income taxes — Michigan Business Tax (MBT) - In July 2007, the MBT was enacted by the State of Michigan. State

deferred tax liabilities were established, and offsetting regulatory assets were recorded as the impacts of the deferred tax

liabilities will be reflected in rates.

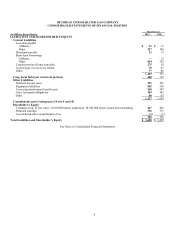

LIABILITIES

• Asset removal costs — The amount collected from customers for the funding of future asset removal activities.

• Refundable income taxes — Income taxes refundable to MichCon’ s customers representing the difference in property-related

deferred income taxes payable and amounts recognized pursuant to MPSC authorization.

• Accrued GCR refund — Liability for the temporary over-recovery of and a return on gas costs incurred by MichCon which are

recoverable through the GCR mechanism.

• Safety and training cost refund — The MPSC ordered the refund of unspent costs which were included in the Company’ s rates.

• Accrued pension — Pension expense refundable to customers representing the difference created from volatility in the pension

obligation and amounts recognized pursuant to MPSC authorization.

• Deferred income taxes — Michigan Business Tax — In July 2007, the MBT was enacted by the State of Michigan. State

deferred tax assets were established, and offsetting regulatory liabilities were recorded as the impacts of the deferred tax assets

will be reflected in rates.

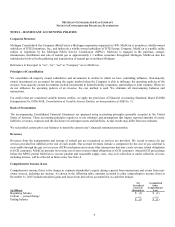

Regulatory Accounting Treatment for Performance Excellence Process

In May 2006, we filed applications with the MPSC to allow deferral of costs associated with the implementation of the Performance

Excellence Process, a company-wide cost-savings and performance improvement program. Implementation costs include project

management, consultant support and employee severance expenses. We sought MPSC authorization to defer and amortize

Performance Excellence Process implementation costs for accounting purposes to match the expected savings from the Performance

Excellence Process program with the related CTA. We anticipate the Performance Excellence Process to continue into 2008. Our CTA

is estimated to total between $55 million and $60 million. In September 2006, the MPSC issued an order approving a settlement

agreement that allows commencing in 2006, to defer the incremental CTA. Further, the order provides for us to amortize the CTA

deferrals over a ten-year period beginning with the year subsequent to the year the CTA was deferred. However, we cannot defer CTA

costs at this time because a recovery mechanism has not been established. We expect to seek a recovery mechanism in our next rate

case in 2009.

Uncollectible Expense True-Up Mechanism (UETM) and Report of Safety and Training-Related Expenditures

2005 UETM — In March 2006, MichCon filed an application with the MPSC for approval of its UETM for 2005. This is the first

filing MichCon has made under the UETM, which was approved by the MPSC in April 2005 as part of MichCon’ s last general rate

case. MichCon’ s 2005 base rates included $37 million for anticipated uncollectible expenses. Actual 2005 uncollectible expenses

totaled $60 million. The true-up mechanism allows MichCon to recover ninety percent of uncollectibles that exceeded the $37 million

15