DTE Energy 2009 Annual Report Download - page 15

Download and view the complete annual report

Please find page 15 of the 2009 DTE Energy annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

|

|

13

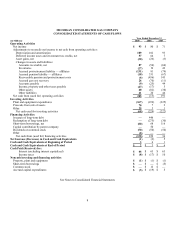

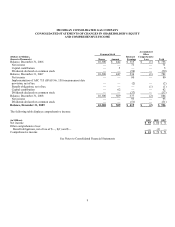

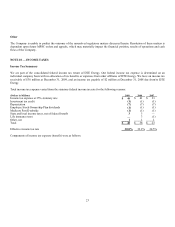

Subsequent Events

The Company has evaluated subsequent events through March XX, 2010, the date that these financial statements were issued.

Other Accounting Policies

See the following notes for other accounting policies impacting the Company’ s consolidated financial statements:

Note

Title

3

New Accounting Pronouncements

4

Fair Value

5

Financial and Other Derivative Instruments

7

Asset Retirement Obligation

9

Regulatory Matters

10

Income Taxes

15

Retirement Benefits and Trusteed Assets

NOTE 3 — NEW ACCOUNTING PRONOUNCEMENTS

FASB Accounting Standards CodificationTM(Codification)

On July 1, 2009, the Codification became the single source of authoritative nongovernmental generally accepted accounting principles

(GAAP) in the United States of America. The Codification is a reorganization of current GAAP into a topical format that eliminates

the current GAAP hierarchy and establishes two levels of guidance — authoritative and non-authoritative. According to the FASB, all

“non-grandfathered, non-SEC accounting literature” that is not included in the Codification would be considered non-authoritative.

The FASB has indicated that the Codification does not change current GAAP. Instead, the proposed changes aim to (1) reduce the

time and effort it takes for users to research accounting questions and (2) improve the usability of current accounting standards. The

Codification is effective for interim and annual periods ending after September 15, 2009.

Fair Value Accounting, Measurements and Disclosure

In September 2006, the FASB issued ASC 820 (SFAS No. 157, Fair Value Measurements). The standard defines fair value,

establishes a framework for measuring fair value in generally accepted accounting principles, and expands disclosures about fair value

measurements. It emphasizes that fair value is a market-based measurement, not an entity-specific measurement. Fair value

measurement should be determined based on the assumptions that market participants would use in pricing an asset or liability.

Effective January 1, 2008, the Company adopted ASC 820 (SFAS No. 157). As permitted by ASC 820-10 (FSP No. 157-2), the

Company elected to defer the effective date of the standard as it pertains to measurement and disclosures about the fair value of non-

financial assets and liabilities made on a nonrecurring basis. The Company has adopted the recognition provisions for non-financial

assets and liabilities as of January 1, 2009. See Note 4.

In April 2009, the FASB issued three FSPs intended to provide additional application guidance and enhance disclosures regarding fair

value measurements and impairments of securities. The FSPs are effective for interim and annual periods ending after June 15, 2009.

• ASC 825-10 (FSP No. 107-1 and APB No. 28-1), Interim Disclosures about Fair Value of Financial Instruments, expands the

fair value disclosures required for all financial instruments within the scope of ASC 825-10 to interim periods.

• ASC 820-10 (FSP No. 157-4), Determining Fair Value When the Volume and Level of Activity for the Asset or Liability Have

Significantly Decreased and Identifying Transactions That Are Not Orderly, which applies to all assets and liabilities, i.e.,

financial and nonfinancial, reemphasizes that the objective of fair value remains unchanged (i.e., an exit price notion). The FSP

provides application guidance on measuring fair value when the volume and level of activity has significantly decreased and