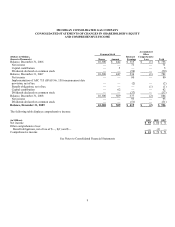

DTE Energy 2009 Annual Report Download - page 16

Download and view the complete annual report

Please find page 16 of the 2009 DTE Energy annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

|

|

14

identifying transactions that are not orderly. The FSP also emphasizes that an entity cannot presume that an observable

transaction price is not orderly even when there has been a significant decline in the volume and level of activity.

• ASC 320-10 (FSP No. 115-2 and SFAS No. 124-2), Recognition and Presentation of Other-Than-Temporary Impairments, is

intended to bring greater consistency to the timing of impairment recognition, and provide greater clarity to investors about the

credit and noncredit components of impaired debt securities that are not expected to be sold.

The Company adopted these FSPs in the second quarter of 2009. The adoption of these FSPs did not have a significant impact on

MichCon’ s consolidated financial statements.

In September and August 2009, respectively, the FASB issued ASU 2009-12, Fair Value Measurements and Disclosure, and ASU

2009-05, Measuring Liabilities at Fair Value. ASU 2009-12 provides guidance for the fair value measurement of investments in

certain entities that calculate the net asset value per share (or its equivalent) determined as of the reporting entity’ s measurement date.

Certain attributes of the investment (such as restrictions on redemption) and transaction prices from principal-to-principal or brokered

transactions will not be considered in measuring the fair value of the investment. The amendments in this standard are effective for

interim and annual periods ending after December 15, 2009.

ASU 2009-05 provides guidance on measuring the fair value of liabilities under ASC 820. This standard clarifies that in the absence of

a quoted price in an active market for an identical liability at the measurement date, companies may apply approaches that use the

quoted price of an investment in the identical liability or similar liabilities traded as assets or other valuation techniques consistent

with the fair-value measurement principles in ASC 820. The standard permits fair value measurements of liabilities that are based on

the price that a company would pay to transfer the liability to a new obligor. It also permits a company to measure the fair value of

liabilities using an estimate of the price it would receive to enter into the liability at that date. The new standard is effective for interim

and annual periods beginning after August 27, 2009 and applies to all fair-value measurements of liabilities required by GAAP. The

adoption of ASU 2009-12 and ASU 2009-05 did not have a material impact on MichCon’ s consolidated financial statements.

In January 2010, the FASB issued ASU 2010-06, Improving Disclosures about Fair Value Measurements. ASU 2010-06 requires the

gross presentation of activity within the Level 3 fair value measurement roll forward and details of transfers in and out of Level 1 and

2 fair value measurements. The new disclosures are required of all entities that are required to provide disclosures about recurring and

nonrecurring fair value measurements. ASU 2010-06 is effective for interim and annual reporting periods beginning after

December 15, 2009, except for the gross presentation of the Level 3 fair value measurement roll forward which is effective for annual

reporting periods beginning after December 15, 2010 and for interim reporting periods within those years.

Disclosures about Derivative Instruments and Guarantees

In March 2008, the FASB issued ASC 815-10 (SFAS No. 161, Disclosures about Derivative Instruments and Hedging Activities — an

amendment of FASB Statement No. 133). This standard requires enhanced disclosures about an entity’ s derivative and hedging

activities and thereby improves the transparency of financial reporting. Entities are required to provide enhanced disclosures about

(a) how and why an entity uses derivative instruments, (b) how derivative instruments and related hedged items are accounted for

under ASC 815 (SFAS No. 133) and its related interpretations, and (c) how derivative instruments and related hedged items affect an

entity’ s financial position, financial performance, and cash flows.

The standard is effective for financial statements issued for fiscal years and interim periods beginning after November 15, 2008, with

early application encouraged. Comparative disclosures for earlier periods at initial adoption are encouraged but not required. The

Company adopted the standard effective January 1, 2009. See Note 5.

Transfers of Financial Assets

In June 2009, the FASB issued ASU 2009-16 (SFAS No. 166, Accounting for Transfers of Financial Assets — an amendment of FASB

No. 140). This standard amends ASC 860, (SFAS No. 140), eliminates the concept of a “qualifying special-purpose entity” (QSPE)

and associated guidance and creates more stringent conditions for reporting a transfer of a portion of a financial asset as a sale. ASU