HSBC 2013 Annual Report Download - page 6

Download and view the complete annual report

Please find page 6 of the 2013 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

|

|

HSBC BANK CANADAHSBC BANK CANADA

4

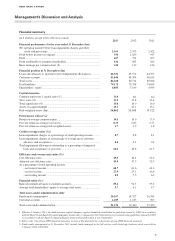

Management’s Discussion and Analysis (continued)

Use of non-IFRS financial measures

In measuring our performance, the financial measures

that we use include those which have been derived from

our reported results. However these are not presented

within the Financial Statements and are not defined

under IFRS. These are considered non-IFRS financial

measures and are unlikely to be comparable to similar

measures presented by other companies. The following

non-IFRS financial measures are used throughout

this document and their purposes and definitions are

discussed below:

Performance ratios

Performance ratios are useful for management to evaluate

profitability on equity, assets and risk-weighted assets.

Return on average common equity is calculated

as annual profit attributable to common shareholders

divided by average common equity (determined using

month-end balances).

Post-tax return on average assets is calculated as annual

profit attributable to common shareholders divided by

average assets (determined using average daily balances).

Post-tax return on average risk-weighted assets is

calculated as profit attributable to common shareholders

divided by the average monthly balances of risk-

weighted assets for the year. Risk-weighted assets are

calculated using guidelines issued by OSFI in accordance

with the Basel II and III capital adequacy frameworks

(2012 and 2011: Risk weighted assets are calculated

using the guidelines issued by OSFI in accordance with

the Basel II capital adequacy framework).

Efficiency ratios

Efficiency ratios are measures of the bank’s efficiency

in managing its operating expense to generate revenue.

Cost efficiency ratio is calculated as annual total

operating expenses as a percentage of annual net

operating income before loan impairment charges and

other credit risk provisions.

Adjusted cost efficiency ratio is calculated similar to

the cost efficiency ratio; however, annual net operating

income before loan impairment charges and other credit

risk provisions excludes annual gains and losses from

financial instruments designated at fair value, as the

movement in value of the bank’s own subordinated debt

issues primarily driven by changes in market rates and

are not under the control of management.

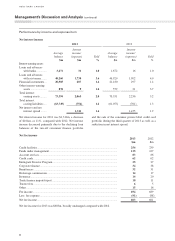

Revenue mix ratio

This measure demonstrates the contribution of each of

the primary revenue streams to total income.

Net interest income, net fee income and net trading

income as a percentage of total operating income is

calculated as annual net interest income, annual net fee

income and annual net trading income divided by annual

net operating income before loan impairment charges

and other credit risk provisions.

Financial ratios

These measures are indicators of the stability of the

bank’s balance sheet and the degree funds are deployed

to fund assets.

Ratio of customer advances to customer accounts is

calculated by dividing loans and advances to customers

by customer accounts using year-end balances.

Average total shareholders’ equity to average total

assets is calculated by dividing average total shareholders’

equity for the year (determined using month-end

balances) with average total assets (determined using

daily balances) for the year.

Assets under administration

These are assets administered by the bank on behalf of

our customers. The bank does not recognize these assets

on its consolidated statement of financial position because

our customers are the beneficial owners. This indicator

demonstrates the bank’s ability to earn net fee income.